UK Investment Trusts in 2026: Governance Under Pressure

Ahmed Suliman & Oliver Taylor

In Collaboration with Nepean

Introduction

2025 marked a decisive shift in the UK investment trust landscape. What began as a prolonged period of wide discounts evolved into a sustained test on balance sheets, permeating into corporate governance, as boards were increasingly required to demonstrate that the closed-ended structure continued to serve shareholder interests.

At the centre of this shift was a series of high-profile activist campaigns led by Saba Capital, whose actions since late 2024 have reshaped expectations around board accountability, corporate actions, and shareholder engagement across the sector.

Our analysis examines these developments through a governance, M&A, and activism lens, highlighting how shareholder expectations have evolved and why boards are increasingly judged on their ability to deliver tangible outcomes within the closed-ended structure. Alongside this, Nepean’s contribution provides a complementary perspective on the strategic communication challenges facing boards, particularly in the context of the Saba campaigns.

Activism in Focus: Saba Capital’s Campaigns (Late-2024 to 2025)

Since the end of 2024, Saba Capital has mounted coordinated campaigns across multiple UK investment trusts, seeking outcomes ranging from board change and enhanced discount-control mechanisms to structural reform, including mergers, wind-ups, or conversion to open-ended vehicles.

While many of Saba’s formal resolutions were ultimately defeated, the broader impact of these campaigns has been significant. The activism demonstrated that:

- large shareholders are prepared to challenge the legitimacy of the closed-ended structure where discounts persist;

- board composition, tenure, and responsiveness are now regularly challenged; and

- corporate actions once considered exceptional are increasingly viewed as normal.

For issuers, the key lesson is that “Winning the vote” is no longer the end-game. Even unsuccessful activist campaigns have materially influenced board behaviour, disclosure standards, and strategic positioning. Activists are also focusing on their financial returns, which they believe will be enhanced by making changes to the governance structure of funds.

Developments since 2025 suggest a further escalation. Activism is no longer limited to proposing change, but increasingly about controlling outcomes. Large shareholders have demonstrated their ability to block strategic transactions, including mergers. They have also shown the ability to shape board decisions indirectly through ownership concentration. Overall, the events represented a meaningful shift in board dynamics. It is also a reminder that activism can evolve from persuasion to leverage.

Net Asset Value (NAV) Discounts as a Governance Indicator

Perhaps the most enduring theme of 2025 was the treatment of discounts to Net Asset Value (NAV) as a live measure of governance quality. For investment trusts, the market’s message was clear:

- persistent discounts are no longer seen as a purely cyclical or technical issue;

- they are interpreted as a reflection of board effectiveness, engagement quality, and structural credibility.

Where discounts remain elevated despite buybacks and engagement, investors are increasingly questioning whether the closed-ended structure itself remains appropriate.

The Impact of US-Style Activism on UK Investment Trust Sector

Saba’s role is particularly noteworthy given its identity as a US-based hedge fund exerting influence over UK-listed investment trusts. This has introduced several new dynamics into the market:

- A different activism playbook: Unlike traditional UK stewardship-led engagement, Saba’s approach has been more overtly transactional and structural, framing persistent discounts as evidence of governance failure rather than market conditions. This has accelerated the pace at which boards are expected to respond.

- Shareholder concentration risk: Saba’s campaigns highlighted how significant minority stakes can be leveraged to block or influence corporate actions, including mergers. This has sharpened boards’ focus on developing a more granular understanding of their shareholder base and the risks associated with concentrated ownership.

- Market-wide signalling effect: Even where Saba did not prevail, its campaigns signalled to other investors that boards can be challenged and that the investment trust sector is increasingly open to activist intervention.

Implications for Boards and Issuers

As a result, issuer expectations have shifted: boards are now expected to anticipate activism, not merely respond to it. The experience of 2025 suggests that inaction is now the highest-risk strategy. The developments across 2025 give rise to several clear governance implications:

- Engagement must be proactive, not reactive: Waiting for an activist requisition before engaging shareholders is no longer sufficient. Boards are expected to demonstrate a deep understanding of strategy and the systemic risks to the funds.

- Structural questions cannot be deferred indefinitely: Where discounts persist despite buybacks and engagement, boards should expect pressure to consider more fundamental options, including consolidation or conversion.

- Corporate actions require activist-proofing: M&A proposals must be stress-tested against shareholder fairness, mandate alignment, and value transfer optics.

- Shareholder register monitoring is critical: Understanding who holds influence—and how that influence might be exercised—has become a core governance responsibility

- Structural changes must be considered for contingency: Boards should not wait until pressure escalates to consider alternatives such as mergers, wind-downs, or structural change.

Conclusion: 2025 as an Inflection Point

For UK investment trusts, 2025 was an inflection point. Developments into 2026 suggest it is becoming something more — a structural reset in governance expectations.

The combination of sustained activism, persistent discounts, and increasingly contested corporate actions has fundamentally altered how boards are assessed.

For issuers, the lesson is not that activism must always be resisted or conceded, but that credible governance, clear strategy, and early engagement are now essential defences. In these events, governance is measured by how well the board translates strategy into fruitful shareholder outcomes.

As the sector moves forward, boards that can articulate why the closed-ended model works, and how they will protect shareholder value within it, will be best placed to navigate the next phase of scrutiny.

Independent Strategic Communications Advice for Boards: Lessons from the Saba 7

For a few unfortunate investment trust boards, Saba was the Grinch that stole Christmas of 2024. But, if they’d hoped that it was a passing challenge, events since will have left them sadly mistaken.

The saga has persisted for more than a year. Whilst boards and their investment trusts have not sat still, activist threats remain and further challenges arising from investor demographic shifts continue to mount.

Below, we explore what boards learnt from their initial threat exposure, and what they should consider to traverse the hurdles ahead.

The Visibility Gap

Our review (in-post) of the trusts revealed a consistent pattern: boards with low public visibility – limited LinkedIn activity, minimal proactive media engagement, and absent or outdated standalone websites – were generally less well prepared when activist pressure emerged.

Of course, having effective and efficient storytelling channels in place is unlikely to have prevented the Saba challenge itself. Rather, we believe the lack of greater preparedness meant tackling the challenge once established became harder – and would have been harder still had Saba opted to pick off individual trusts rather than a collective.

Of the Saba 7, most had no LinkedIn presence in the period preceding the requisition, with little evidence of targeted engagement from board members to relevant stakeholders. Trusts largely communicated through RNS announcements, with scarce use of digital channels. When activist scrutiny intensified, these boards lacked official means through which to communicate with the broad investor base.

Most board members at the time of the requisition were found to have established channels on LinkedIn. However, posts about their respective trusts were minimal – only to be ramped up ahead of the requisitioned meetings.

The Cost of Reactive Governance

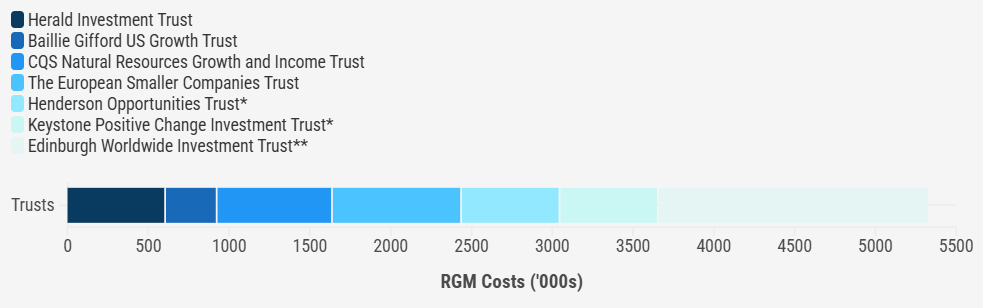

These requisition processes did not come cheap, and we think it is reasonable to suggest that such costs were heightened by the lack of a comprehensive, pre-existing route to communicating with shareholders.

* Henderson Opportunities Trust and Keystone Positive Change Investment Trust have not disclosed their fees due to their voluntary liquidations. Figures above are an average of other trusts’ costs where clearly disclosed.

** Edinburgh Worldwide Investment Trust recorded £1.673 million in non-recurring expenses, comprising costs associated with the February requisitioned general meeting and ‘legal costs incurred in connection with the cancellation of the share premium account’.

Four of the seven trusts recorded cumulative additional expenses of £2.58 million in their subsequent annual reports, accrued in relation specifically to those single requisitioned meetings. The others have either not disclosed their fees* or have reported fees in combination with other related costs†.

These are not insignificant figures, and fees accrued at shareholders’ expense – something we know Board members, with their focus on shareholders’ interests, are acutely aware of.

Prevention is better than cure, but a cure is still preferable to emergency surgery. And cheaper, too.

The Retail Challenge

Investment trusts are operating in an increasingly challenging environment. Their traditional investor base is ageing, while younger generations are gravitating towards alternative investment products and have markedly different expectations regarding communication and engagement. At the same time, the sector continues to face persistent structural pressures: widening discounts, consolidation among wealth managers, and growing competition from a broader universe of investment products.

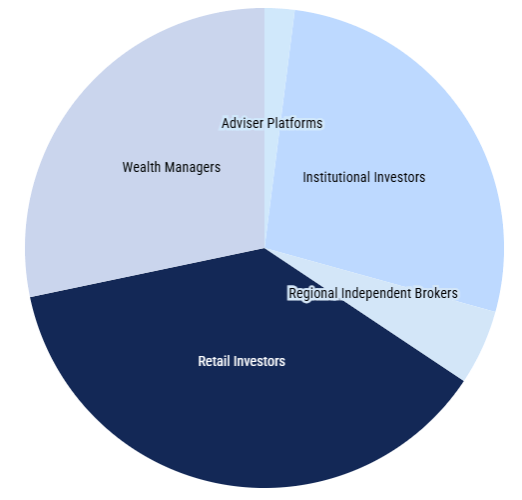

Private investors are central to the sector± – accounting for over a third of total shareholdings by value – and their influence is increasing as retail participation rises across UK markets. And yet, there is still a limited understanding among many retail investors of what an investment trust is, how it works, and what exactly the role of the board is. This has created both a vulnerability and an opportunity: a need to prepare for expert activists among an increasingly ill-informed investor base, but also a chance to more effectively engage brand new audiences.

The average investment trust shareholder is 60–65 years old§ but, as wealth shifts, this profile will change. The typical future investor will be digitally native and motivated by values – an audience that currently favours other vehicles like ETFs. Lacking the longstanding loyalty of the old guard, they might also be more likely to sympathise with an activist’s calls for change – making critical the need for board independence, if they are to avoid being swept away in a coup.

In a landscape defined by demographic change, increasing retail influence, evolving expectations, and heightened activist pressure, boards must ensure they are not only fulfilling their duties but are visibly doing so.

Building Board Preparedness

For investment trusts, boards serve as the embodiment of shareholders’ interests. They are their independent, accountable representatives, and the experts entrusted with governance and critical oversight.

We believe there is a significant opportunity for boards to raise their voice and be more proactive by building their platform to communicate to shareholders. Modern challenges require modern solutions, and the demands of an increasingly critical retail investor base have to be met – particularly in the face of activist threats.

The successful transmission of board messages greases the wheels of action. It can allow them to better hold investment managers to account and allow for more productive engagement with activists – particularly when those activists are supported by a broader group of shareholders. In getting these messages across, digital methods in particular are currently underutilised.

Independent of investment managers, board members should build their own digital profiles – both individually and at the trust-level. Personalisation is a route to ownership of accountability: a counter to criticism levelled at investment trust by Saba and others.

Our research suggests that LinkedIn is one platform in particular where boards can be doing more, alongside use of video content, independent websites, and targeted engagement with the press.

In combination with other forms of shareholder engagement, such as proxy solicitation, it is a route to a more comprehensive communications strategy: traversing the width of the shareholder map and meeting the needs of the full breadth of shareholders, big and small.

Raising Their Voice

Since Saba’s original challenge, boards have come a long way. It was a wake-up call, and one that many have answered. Today, as we have seen in recent weeks and months, they’re fighting back – and winning, too. But this is a challenge – both in responding to activists and in adjusting to an increasingly retail-led investor base – that is going nowhere.

Boards need a voice: one that is independent of investment managers, loud enough to reach retail investors, and clear and distinct in its delivery.

This is not an exercise in vanity. Building a communications platform is a route to more effective positioning and protection. It means reaching the full breadth of shareholders in decision-making moments; being prepared for the current and future challenges that are shaping the sector; and driving cost-savings in contentious situations, to all shareholders’ benefit.

Only with such a voice can boards be confident in their position in the moments that matter.

Alliance Advisors Team

At Alliance Advisors, we support our EMEA-clients on each assignment with a dedicated global team that consists of:

Citations

* Henderson Opportunities Trust and Keystone Positive Change Investment Trust have not disclosed their fees due to their voluntary liquidations.

† Edinburgh Worldwide Investment Trust recorded £1.6 million in non-recurring expenses, comprising costs associated with the February requisitioned general meeting and ‘legal costs incurred in connection with the cancellation of the share premium account’.