European Proxy Season 2025 Review

The Great Calibration

Foreword

For the past three years, Alliance Advisors has had the privilege of guiding listed companies across EMEA in preparing for their Annual General Meetings.

Though relatively new to the market, we have forged an alliance of seasoned professionals, market specialists, and emerging talent—united by a shared commitment to delivering a truly distinguished client experience.

As one client graciously observed: “You anticipate questions our board, legal, or investor relations colleagues have not yet considered.”

It is precisely this blend of insight, creativity, and meticulous attention that defines our approach to governance and shareholder engagement.

This Season Review reflects the collective expertise of our team, drawing on our work across the United Kingdom, Germany, Switzerland, Austria, and Spain. It provides a considered overview of the 2025 Shareholder Meeting Season -the triumphs, the challenges, and the notable trends- and offers our perspective on the forthcoming 2026 season.

Particular attention is given to ESG and Sustainability reporting across the region. While investors have streamlined their guidelines in response to the evolving political landscape, they are exercising heightened scrutiny regarding the quality and integrity of disclosures.

Board composition, qualifications, and independence continue to be the primary drivers of shareholder dissent. However, the rationale for opposition is evolving, with increased focus on committee effectiveness, responses to previous shareholder concerns, and preparedness for both short- and long-term strategic imperatives.

Remuneration matters remain closely examined, with the United Kingdom, in particular anticipating a new wave of policies for shareholder consideration.

We hope you enjoy this edition, and we invite you to remain engaged with our team’s weekly updates via our dedicated news channel.

Tom & Angelika

Executive Summary

2025 AGM Season Review

Across Europe, the 2025 proxy season showed familiar patterns of combined high routine support with sharper dissent concentrated in executive pay and selected director elections. This was uncovered through the AGM landscape, where voting behavior revealed much, including familiar patterns and hidden gems.

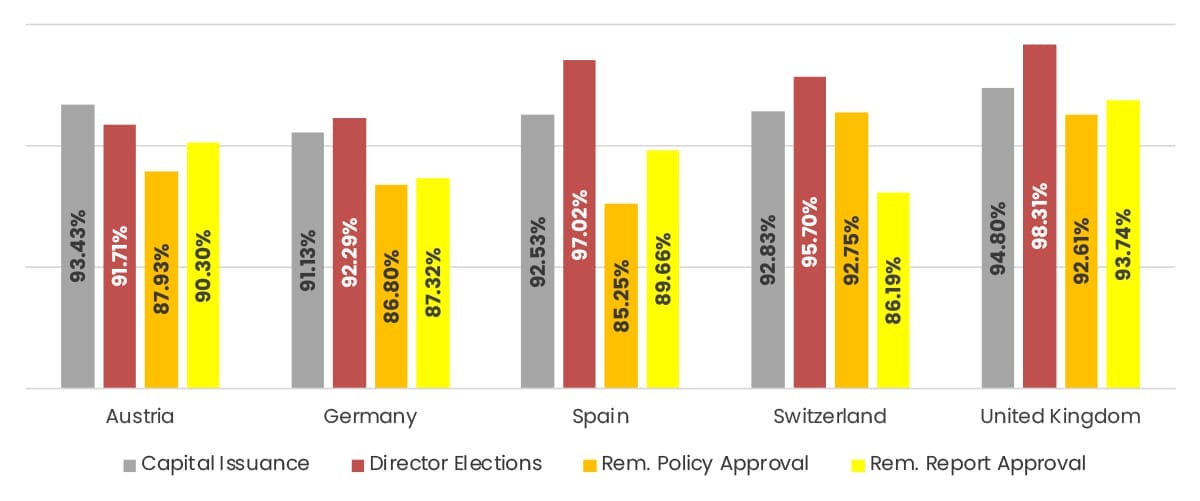

2025 Avg. Support Levels – Per Category

Germany. Outcomes diverged by the different indices. DAX issuers continued to clear most items comfortably, but MDAX/SDAX companies experienced materially higher “Against” rates and lower average support on remuneration reports and new/renewed policies. Virtual-AGM mandates became a live fault line at a few large names, underlining how meeting format decisions can influence investor sentiment.

United Kingdom. Across all markets, average support was highest in 3 out of the 4 focal items. However, outliers on remuneration reports and policies highlighted investor intolerance for windfalls, uneven disclosure and weak performance alignment.

Austria. Headline voting remained calm. Discharge and routine items continued to pass with strong margins, yet pay items drew comparatively elevated scrutiny. The pattern suggests investors want tighter calibration (metric choice, target setting, caps, and a clearer account of realizable pay) even where overall support remains comfortable.

Switzerland. Routine consensus remained strong, while investor coalitions kept pay fairness, independence, and ESG disclosure in focus.

Spain. Approvals were high across especially for director elections. There were pockets of pressure on pay and growing attention to board parity and AI oversight.

European Trends

Pay Calibration in Focus

Across markets, remuneration remains the most contentious and scrutinized topic. Voting behavior reveals that investors are converged on a single expectation: show the business problem the plan solves, the rationale for chosen metrics, the benchmarks (caps, malus/clawback), and the realizable pay under credible scenarios. Mid-cap German and Austrian issuers are particularly exposed where the rationale is vague or structures permit excessive or unwarranted payouts. UK and Swiss investors consistently demand for clearer links between outcomes and performance, with limited patience for retrospective rationales or mid-cycle resets.

Rise of Beneficiary Voting Among Large Managers

A structural shift is the scaling of beneficiary voting choice, which redistributes a slice of voting power away from central stewardship teams to end-investors. BlackRock were key in putting this trend to the mainstream when they launched the BlackRock Voting Choice in 2022, where clients can default to BlackRock or select third-party policy sets. As of June 30, 2025, they report that clients representing about $784bn in AUM were actively exercising policy choices. State Street Global Advisors expanded Proxy Voting Choice in 2025 (including European SICAVs), offering multiple third-party policy menus and reporting strong take-up. Vanguard materially widened Investor Choice in May–September 2025 to 12 index funds, bringing eligible assets to nearly $1 trillion and reach to 10 million investors, with participation more than doubling year-on-year.

For European issuers, the short-term goal is greater dispersion around mean outcomes, particularly on remuneration and E&S-linked items, as subsets of beneficiaries adopt different policies. Despite the levels of opt-in rates, even smaller level participation on very large AUM can tilt close votes. Issuers should therefore complement traditional stewardship engagement with segments thoroughly tailored to addressing common beneficiary policy issues.

Evidence-based Stewardship and Controls

The UK’s outcomes-oriented stewardship reporting and the incoming internal-controls declaration (for FYs starting 1 January 2026) are already shaping investor expectations across Europe. Boards should assume their assertions will be tested against audit, risk, and internal-control evidence packs, with an emphasis on scope, testing methodology and third-party assurance. Even outside the UK, this standard is becoming the practical benchmark for credibility.

Meeting Format is now Strategic

German votes on virtual-AGM mandates showed that format choices carry reputational and voting risk. Issuers with complex or sensitive items (new pay policies, contested elections, significant capital asks) may benefit from physical or hybrid formats to demonstrate openness to challenge and to manage perception risk.

The ESG Shift: From Aspiration to Execution

Across markets, investor focus moved from broad ESG narratives to assurance-ready, decision-useful disclosure. CSRD/ESRS has effectively turned sustainability reporting into a controls exercise by enforcing boards to evidence data lineage, audit trails, and third-party assurance—especially for climate metrics, supply-chain emissions, and social KPIs. Where disclosure quality is lacking or methodologies aren’t reproducible, scrutiny now travels through governance frameworks (committee chair and board votes) rather than E&S proposals. Support for environmental and social resolutions declined, but stewardship intensity rose via targeted engagement, with large managers rewarding issuers that present transition plans and credible interim milestones.

Germany

DAX, MDAX & SDAX

AGM Format Takes Center Stage

Introduction

Germany is one of the few jurisdictions worldwide where a two-tier board is the rule where a non-executive Supervisory Board (SB) controls the separate executive Management Board. The shareholders only elect the Supervisory Board members, while the Management Board (MB) members, for example the CEO, is appointed by the Supervisory Board.

Although five-year terms are possible, many institutional investors do not support terms exceeding four years. Therefore, the primary way to express criticism during such a multi-year term is to vote against the SB’s discharge. Similarly for the MB, as they are anyway not elected but appointed.

The most followed topic in this proxy season was around the virtual AGM. Due to proxy advisory guidelines and investor pressure, the first authorization two years ago were mostly limited to 2 years.

This season, also connected to a presumed tightening of the relative ISS guidelines, there was a certain uncertainty among companies. As these authorizations for holding virtual AGMs are bylaw-connected votes, different minimum thresholds are applicable. Between the traditional German legal form of the Aktiengesellschaft (Public Limited Company) and the European legal form of the Societas Europaea, such thresholds could be at 50% support, 2/3 or 75%.

Partially, these thresholds can also vary depending on specific deviating rules inside the bylaws. Considering the most important companies inside the DAX family, only two companies failed to achieve the necessary support.

As the vast majority of companies asked again for an authorization for the next two years, this topic will come back with the 2027 AGM season, while companies need to figure out what to do in 2026.

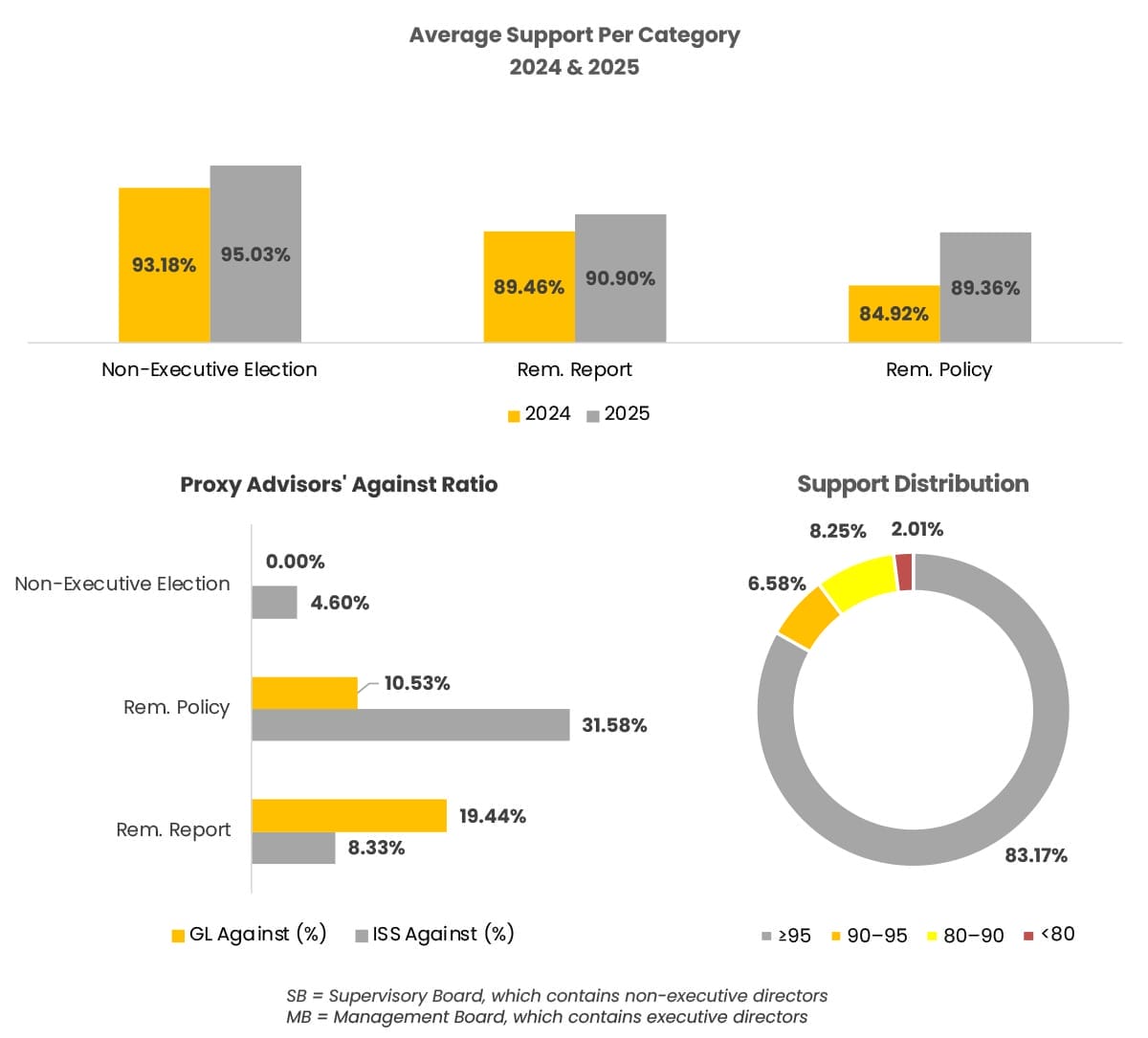

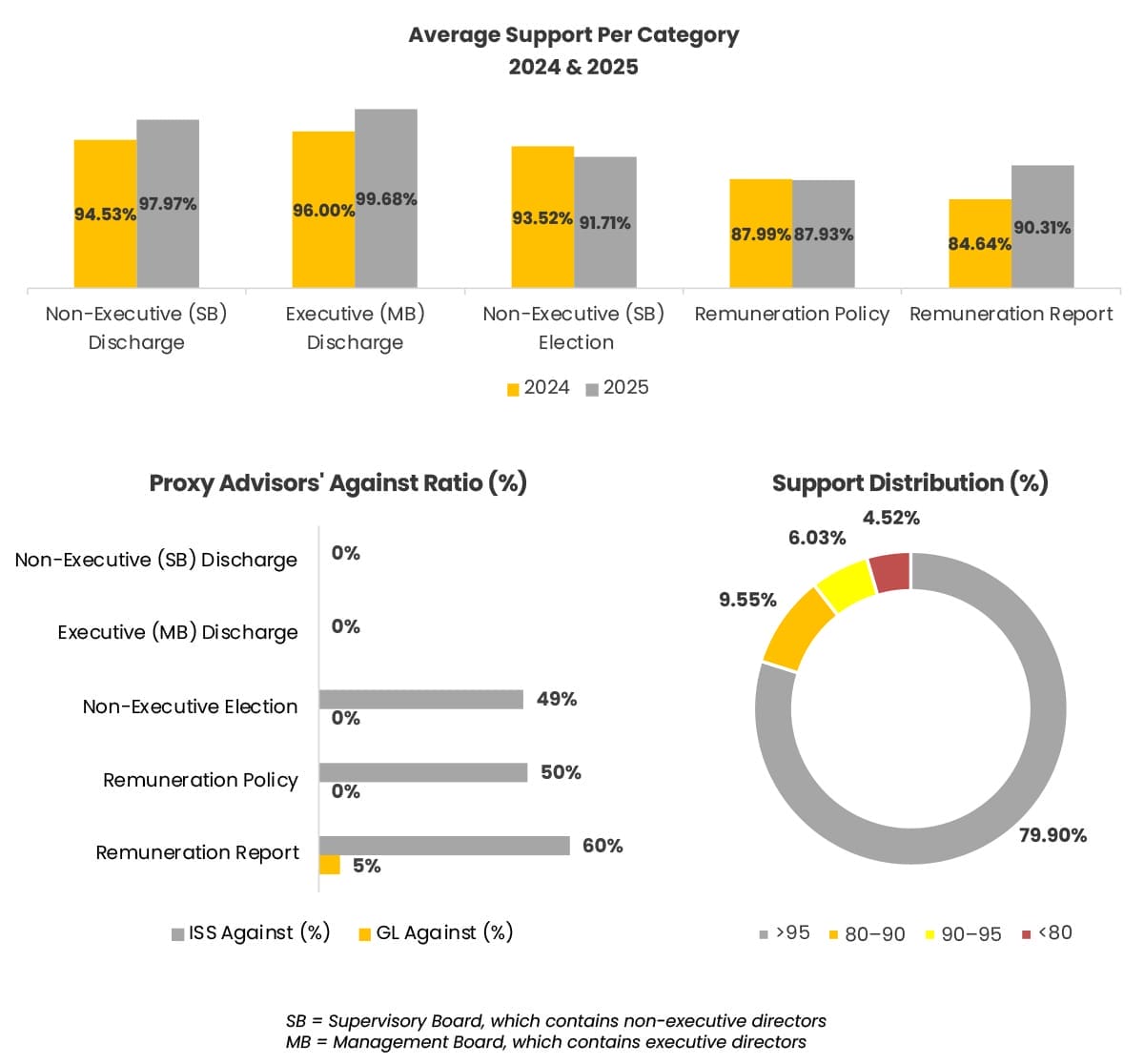

Key AGM Results: DAX

- Non-executive (Supervisory Board) elections analysis shows 36% female candidates vs. 64% male (31 vs. 56).

- 3 of the 36 Remuneration Reports (8%) received a negative ISS recommendation.

- 6 of the 19 Remuneration Policies (32%) received a negative ISS recommendation.

AGM Season Insights: DAX

In 2024 and in 2025, there was a ratio of female and male candidates of roughly 1/3 to 2/3. However, it must be noted that these numbers are somewhat distorted, as the overwhelming number of elected directors have multi-year, usually four-year terms.

We talk about candidates for a board seat, but there is a possibility that the same person is proposed by more than one company. Often, there is no attention for such cases, as there is for the usually applied multi-year terms.

In 2025, we found two cases where the same person stood for nomination at multiple supervisory board mandates:

- Rachel Empey at BMW and at Deutsche Telekom with support levels reaching 98.5% and 99.8% respectively;

- Sigmar Gabriel at Deutsche Bank, Rheinmetall & Siemens Energy with support levels reaching 95.6% and 99.3% respectively;

The remuneration topic is divided into two different findings.

The Remuneration Reports stays low in ISS-against ratios, with only 8% in 2025 of 36 Reports, in line with 2024 where ISS was against 9% out of 35 different Reports.

Similarly, the support rates of around 90% in both years and the lowest approval at 67.4% in 2025 against 58.3% in 2024.

The Remuneration Policies, however, present a different picture. 32% of the 19 Systems received a negative ISS-recommendation, whilst the average support was at 89% and the lowest support at 56.7%. Interestingly, in 2024 only 17% of the 12 Policies received a negative recommendation, yet the average support level was nearly identical to 2025, at 89%. The lowest support in 2024 was even less at 40.4%.

Within the DAX, the only company not achieving the necessary support for the renewal of their virtual AGM authorization was Siemens. It was not the company with the lowest support level in the DAX. This means that Siemens is mandated to hold a physical AGM in 2026 due to the expired authorization in their bylaws.

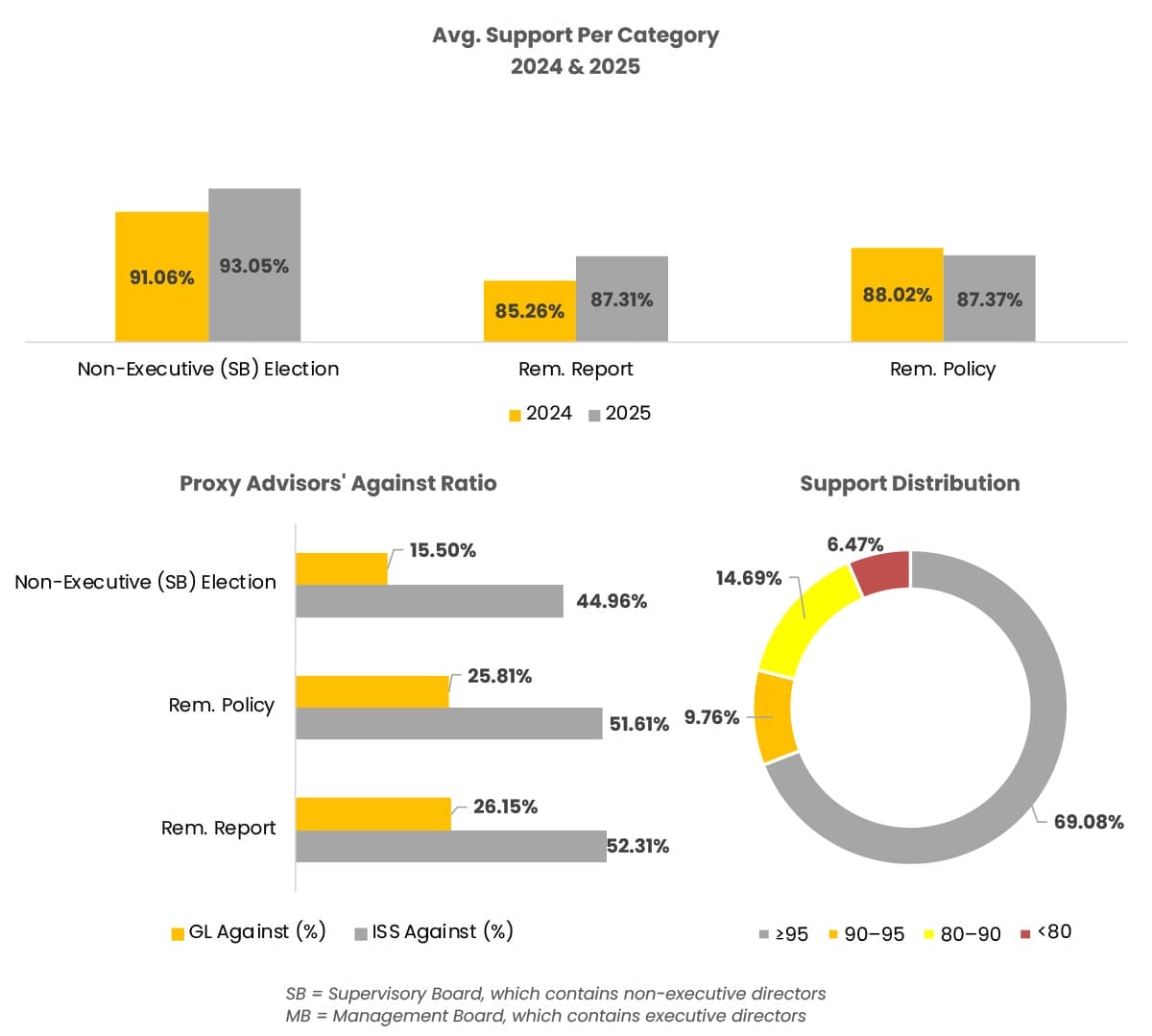

Key AGM Results: MDAX

- Non-executive (Supervisory Board) elections analysis shows 33% female candidates vs. 67% male (27 vs. 56).

- 20 of the 46 Remuneration Reports (44%) received a negative ISS recommendation.

- 10 of the 24 Remuneration Policies (42%) received a negative ISS recommendation.

AGM Season Insights: MDAX

In 2024 and in 2025, there was a ratio of female and male candidates of roughly 1/3 to 2/3. But it must be considered that these numbers are somewhat distorted, as the overwhelming number of elected directors have multi-year, usually four-year terms.

We talk about candidates for a board seat, but it can happen that the same person is proposed by more than only one company. Often, there is no attention for such cases, as for the usually applied multi-year terms.

In 2025, we found one case where the same person ran for more than one supervisory board mandate:

- Stephan Sturm ran for a seat at Hugo Boss and at Knorr Bremse, with support levels between 86.9% and 98.8%.

The remuneration topic, however, raises several warning signs.

Since our first in-depth analysis in 2024, the quota of negative ISS recommendations is at high levels. In 2024, ISS was against 36% of the Remuneration Reports, and this year against 44%. The impact on the voting results is visible. While one Report only achieved 38.9%, the average support is only at 84.5%. This indicates a high degree of misalignment with ISS expectations, which partially overlap with most of the institutional (free float) investors.

Similarly for the Remuneration Policies with 43% negative ISS recommendations in 2024 and 42% in 2025. And with an average support of only 84% and the lowest support of a System at 47.8%, the perception of a certain misalignment continues also here, which is partially comprehensible because up to a certain degree, the Remuneration Report and the Remuneration System depend on each other.

Inside the MDAX, the only company not achieving the necessary support for the renewal of their virtual AGM authorization was TUI. Interestingly, it was not the company with the lowest support level inside the DAX. This means that TUI is mandated to hold a physical AGM in 2026 due to the expired authorization in their bylaws.

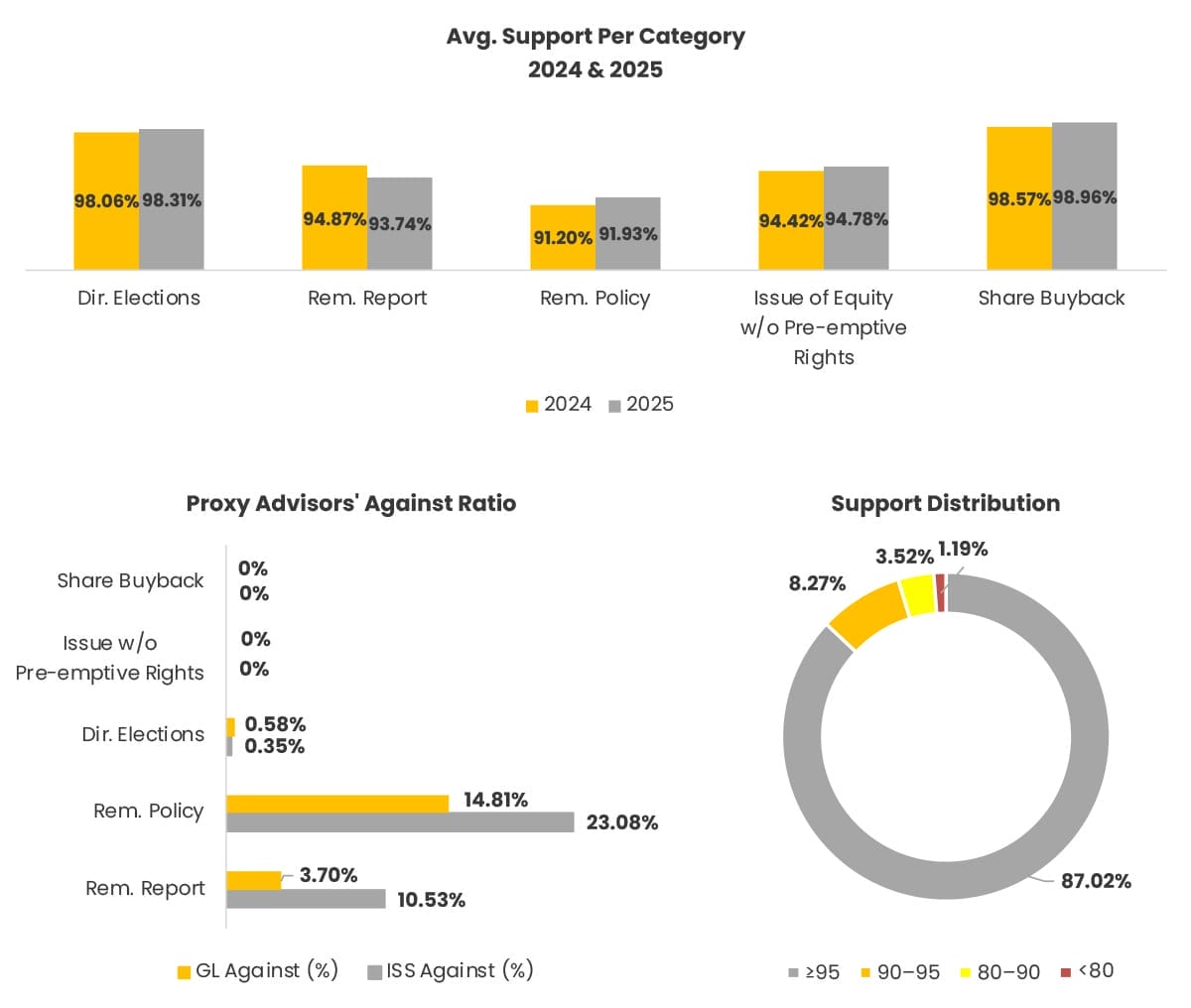

Key AGM Results: SDAX

- Non-executive (Supervisory Board) elections analysis shows 28% female candidates vs. 72% male (37 vs. 94).

- 34 of the 65 Remuneration Reports (52%) receive a negative ISS recommendation.

- 16 of the 31 Remuneration Policies (52%) receive a negative ISS recommendation.

AGM Season Insights: SDAX

From 2024 to 2025, the ratio of female to male candidates dropped from roughly 1:2 to 1:3. But it must be considered that these numbers are somewhat distorted, as the overwhelming number of elected directors have multi-year, usually four-year terms.

We talk about candidates for a board seat, but it can happen that the same person is proposed by more than only one company. Often, there is no attention for such cases, as for the usually applied multi-year terms.

In 2025, we found no cases of individuals running for multiple supervisory board mandates in the SDAX, unlike in the DAX and MDAX.

The remuneration topic instead raises several warning signs.

Since our first in-depth analysis in 2024, the quota of negative ISS recommendations is at high levels. In 2024, ISS was against 59% of the Remuneration Reports, and this year against 52%. The impact on the voting results is visible. While one Report only achieved 49.6%, the average support is only at 87.53%. It shows a high degree of misalignment with ISS expectations, which at least partially overlap with most of the institutional (free float) investors.

Similarly for the Remuneration Policies with 55% negative ISS recommendations in 2024 and 52% in 2025. And with an average support of only 87.4% and the lowest support of a System at 48.81, the perception of a certain misalignment continues also here, which is partially comprehensible because up to a certain degree, the Remuneration Report and the Remuneration System depend on each other.

Inside the SDAX, all company achieved the necessary support for the renewal of their virtual AGM authorization.

Interestingly, the SDAX contains several particularities relative to the DAX and MDAX.

- Companies founded under the European Societas Europaea (“SE”) framework can opt for a one-tier board system. With Patrizia and GFT Technology, the SDAX contains companies with such a one-tier board system. At Patrizia this also meant that the CEO was elected, too.

- Fielmann elected all eight supervisory board candidates by slate, thus with a single voted agenda item.

- Kontron is an Austrian company. While we usually exclude non-domestic incorporated companies, in their case we opted to include it due to the similarity in legal & corporate governance structures, as well as investor and proxy advisor expectations.

Selection of Available Investor Rationale for Negative Voting Decisions

DAX, MDAX & SDAX

Non-Executive (SB) Election

- A vote AGAINST the director nominee is warranted for lack of diversity on the board.

- The board is not majority independent.

- A vote AGAINST the non-independent board chair.

- We note that 40% of the board’s posts are not filled by underrepresented gender.

- The nominee is a new non-independent director and the level of gender diversity on the board is less than 33%.

Non-Executive Board (SB) Discharges

- The board’s Audit committee should comprise directors who are unquestionably independent and have appropriate qualifications, experience, skills and capacity to effectively contribute to the committee’s work.

- Poor governance practice.

- A vote against is warranted due to corporate governance concerns.

Executive Board (MB) Discharges

- Ongoing investigations

- We do not believe the ratification of management acts is in the best interest of shareholders.

- The discharge resolutions are currently bundled, which does not allow shareholders to target individuals

Remuneration

- Pension contributions would remain at 50% of base salaries, which is considered very high in the context of broader European practices.

- The vesting curve provides for payouts for up to 50%-points underperformance, which is not considered to be rigorous.

- The increased level of flexibility results in less transparency on the pay composition setting and according payouts.

- Short-term incentive opportunity outweighs long-term incentive opportunity.

- A vote AGAINST is warranted because awards are permitted to vest for below median relative performance.

2026 Season Outlook:

DAX, MDAX, & SDAX

Every proxy season is heavily influenced by changes to proxy advisory and institutional investors guidelines.

Considering the recent ISS survey and the covered topics there, changes in their guidelines could include for example stricter rules about overboarding thresholds.

While some companies have a certain degree of protection against free float negative votes due to their ownership structure, some others have less.

Institutional investors will continue to push for an alignment with best practice, their own or their proxy advisors’ guidelines.

While the discharge proposal votes remain a topic not worthy of concerning discussions, both the remuneration and the supervisory board elections show very high numbers in terms of negative ISS recommendations and mixed voting results.

Recurring yearly dissent by investors and proxy advisors makes it necessary to analyze them and to react accordingly, taking the negative feedback into account. Voting results below 80%, and particularly below 75%, necessitate further action if there are to be no further problems.

Another interesting point will be the usage of the virtual AGM format. Depending on the shareholder structure and the received dissent, it is not fully clear how (dissent) investors will react if a company will hold its AGM again in the virtual format.

While this is a relatively new topic in the market, coming up only through Covid pandemic, a close analysis of the situation in this year may help companies to make a fact-based decision about the future usage.

One option that is currently discussed by several of our clients is for example an annual alternation of physical and virtual AGMs. Others instead are considering to use the physical AGM only when important agenda items are to be voted.

Such may for example include (re-)elections of key supervisory board members, such as the Chair, or new remuneration systems. Your consultant should be able to provide you advisory also in this space.

United Kingdom

FTSE 100

Evidence Over Assertion

Introduction

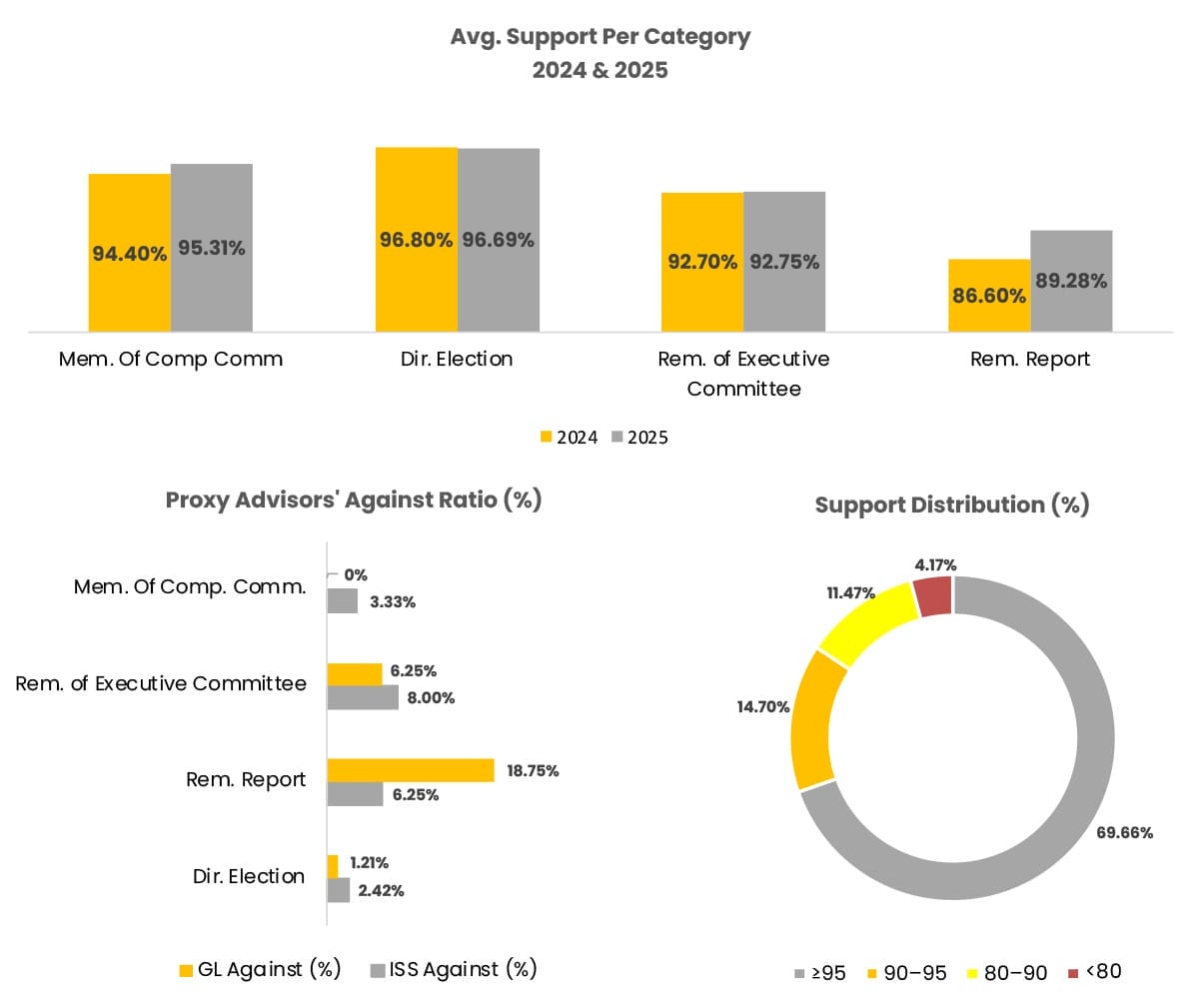

The UK remains a high-standards, shareholder-rights market, anchored by the Corporate Governance Code, the Investment Association’s Public Register discipline at the 20% dissent threshold, and an outcomes-oriented stewardship regime that continues to shape how investors vote and how boards respond.

The 2025 UK proxy season was stable overall, despite moments of volatility. Most routine items sailed through with very high support, yet a visible minority of meetings saw targeted push-back especially on remuneration and a handful of high-profile board elections.

Investors directed their attention on pay design and disclosure, on the accountability of the chair and key committee leads, and on the credibility of internal control narratives ahead of the new controls declaration that applies to financial years beginning 1 January 2026.

Key AGM Results

- Director elections marginally improved. There were notable disparities between male and female candidates.

- Average support for remuneration report approval dropped by 1.13%-points between 2024 to 2025, indicative of a small increase in shareholder scrutiny of retrospective pay practice.

- Remuneration policy approval, support improved modestly by 0.73%-points between 2024 to 2025, suggesting cautious shareholder approval of forward-looking pay frameworks

AGM Season Insights

Executive Remuneration Debate

Executive pay debate re-ignites. FTSE 100 CEO pay hit a record median £4.6m, with more boards paying £10m+ at the top end. This sharpened investor attention on quantum, calibration of LTIs, and fairness narratives, even where vote outcomes remained above 90%. manifest.co.uk

With record CEO pay levels in public view, disciplined communication around fairness and realizable pay will be critical, especially for companies seeking to increase pay quantum or retention awards.

The financial services, specifically the banking sector, went through an adjustment to incentive top talents following the removal of the bonus cap, testing investor patience where increases in variable opportunity were not matched by risk, deferral and claw-back narratives.

BP and Board Accountability

Board accountability was salient topic this year and was represented conspicuously by BP, where investors channeled their concerns about the pace and presentation of strategic shifts through the chair’s re-election. That vote was about more than climate policy as it signaled that for many holders, the director ballot has become the preferred escalation route when they perceive a gap between strategy, delivery and dialogue.

Provision 29 and Tighter Controls

One of the most significant forms of regulatory update comes in the form of a change in reporting and control, which has shifted from boilerplate to board-room due to the incoming internal-controls declaration, Provision 29. Boards should be preparing detailed frameworks in advance (scope, design, testing, assurance options).

UK Stewardship Code 2026

Stewardship reporting intensifies. Once the UK Stewardship Code 2026 is in effect, signatories move to a two-part regime (periodic policy/context + annual activities/outcomes), raising the bar on voting rationale and engagement transparency, pressure that will flow through to issuer dialogues.

With UK investors expected to produce more outcomes-focused Stewardship reports, can we expect clearer rationales for “Against” and more consistent follow-through on engagement asks? This would improve the feedback loop ahead of 2026 AGMs.

2026 Season Outlook

The next season will be shaped by both new rules and by how boards apply existing expectations with discipline. Pay policy renewals will return in a heated public climate, with the number of issuers submitting theirs for shareholder approval expected to peak. Boards seeking to raise opportunities or adapt structures will need to showcase shareholder interests to business goals first and show, with numbers, how the chosen design solves it. Why the metrics, why the calibration, what the benchmarks are, and what realizable pay looks like across different scenarios.

Events from this year signify that there will be heightened focus from investors on chair and committee accountability. Where strategic shifts are underway, the chair’s role in the matter will be scrutinized and may need to be as viewed as importantly as the equity story. For years we have seen a shift in the standards held by Remuneration and audit committee chairs.

The IA’s Public Register continues to anchor that discipline; any vote breaching the 20% threshold should be met with a timely explanation, targeted outreach, and a report back before the next AGM that details the changes made. Resolutions appearing on this list tend to leave a blemish that the issuer are encouraged to address to mitigate shareholder concerns.

Finally, controls readiness is set to become a voting issue, not just a disclosure line. By the time annual reports land in early 2026, investors will expect to see a board-level assessment that is scoped, tested and assured. Issuers are advised from early on to make their programs visible by mapping risks to controls, documenting evidence, and aligning internal audit and external assurance.

Austria

ATX 20

Remuneration Dissent in Focus

Introduction

In Austria, a two-tier board is the rule where a non-executive Supervisory Board controls the separate executive Management Board. The shareholders only elect the Supervisory Board members, while the Management Board members appointed.

While multi-year terms are possible, many institutional investors do not support terms of over four years. Not being able to express any criticism or even getting rid of a Supervisory Board member more directly, the (negative) discharge voting is the only way to express criticism.

Key AGM Results

- •Remuneration topics stay at high levels of negative ISS recommendations (50% & 60%). Lowest support at 66.6%. In 2024, similar negative ISS levels occur.

- Not much different the situation at Non-Executive (SB) elections. Nearly half of the candidates received a negative ISS recommendation. Lowest support at 54.3%.

- Both discharge, for Non-Executive (SB) and Executive (MB), without any negative ISS recommendation. Lowest support at 91.3%.

AGM Season Insights

In 2024, there was nearly a parity between male and female non-executive (SB) candidates. But it must be considered that these numbers are somewhat distorted, as the overwhelming number of elected directors have multi-year terms. Therefore, this topic must be seen with a wider time horizon. Even though in 2025 only 23% of the candidates were female and 77% male, in 2024 it was close to parity with 48% vs. 52%.

With such a two-year horizon of 2024 and 2025, the quota of male candidates is at 63%. Therefore, the two-year female quota is at 37%, which is far from parity, but well in line with the legal framework and national corporate governance code, asking of 30% minimum participation of each gender.

We talk about candidates for a board seat, but it can happen that the same person is proposed by more than only one company. Often, there is no attention for such cases, as for the usually applied multi-year terms.

In 2025, we found two cases where the same male individual ran for two different supervisory board seats. In the first case, the candidate received a negative ISS recommendation, while in the second, he was supported by ISS.

The remuneration topic instead raises several warning signs.

Since our first in-depth analysis in 2024, the quota of negative ISS recommendations is at high levels. In 2024, ISS was against 65% of the Remuneration Reports, and this year still against 60%. The impact on the voting results seems limited. While one Report only achieved 66.6%, the average support is still at 90.3%. It nevertheless shows a high degree of misalignment with ISS expectations, which at least partially overlap with most of the institutional (free float) investors.

Similarly for the Remuneration Systems. with 56% negative ISS recommendations in 2024 and still 50% in 2025. And with an average support of only 87.9% and the lowest support of a System at 69.3%, the perception of a certain misalignment continues also here, which is partially comprehensible because up to a certain degree, the Remuneration Report and the Remuneration System depend on each other.

What instead is not a topic in Austria is the discharge voting. With no negative ISS or Glass Lewis recommendations in the past two years, and average support levels of between 94.5% and 99.7% and the lowest support at 91%, no important dissent occurs.

Publicly available negative voting rationale from institutional investors provide a certain inside into some of the most important reasons for negative investor voting in the ATX.

Non-Executive (SB) Election

- The nominee is non-independent, and the board is not sufficiently independent.

- The board should have an appropriate balance of competencies and backgrounds.

- A voting against the current nomination committee chair is also warranted as a signal of concern to the board because the board is insufficiently gender diverse

- The nominee has attended fewer than 75% of expected meetings in the year under review without a satisfactory explanation.

- The nominee holds an excessive number of mandates at listed companies.

Remuneration

- Remuneration paid to management is not in line with performance, disproportionate, or incommensurate in relation to that of comparable businesses.

- Key performance indicators or parameters that influence variable compensation can be retrospectively adjusted.

- Structure of the compensation scheme does not comply with internationally recognized best practice.

- The management board’s pay package remains substantially above what peers are paying. We emphasize that this has been a concern for a number of years, and the company has still failed to adequately address these concerns.

- A vote against has been applied because awards are permitted to vest for below median relative performance which therefore fails the pay for performance hurdle.

- Under the LTI, discretionary adjustments were made without a compelling explanation as to how far values were adjusted or why they were considered reflective of actual performance.

2026 Season Outlook

Every proxy season is highly influenced by proxy advisory and institutional investors guideline changes.

Considering the recent ISS survey and the covered topics there, changes in their guidelines could include for example stricter rules about overboarding thresholds.

While some companies occur with a certain degree of protection against free float negative votes due to their ownership structure, some others have less.

Institutional investors will continue to push for an alignment with best practice, their own or their proxy advisors’ guidelines.

While the discharge proposal votes remain a topic of not worthy of concerning discussions, both the remuneration and the supervisory board elections show very high numbers in terms of negative ISS recommendations and mixed voting results.

Recurring yearly dissent by investors and proxy advisors makes it necessary to analyze them and to react accordingly, taking the negative feedback into account. Voting results less than 80%, particularly below 75%, necessitates further action if there are to be no further problems.

Switzerland

SMI & SMIM

Scrutiny on Pay and ESG

Introduction

Switzerland maintains a distinctive corporate governance framework that blends Anglo-American and Continental European elements. Despite not being subject to the EU’s Shareholder Rights Directive II (SRD II), many Swiss companies voluntarily align with international best practices. This proactive approach has contributed to strong institutional investor support across AGMs.

Key AGM Results

The 2025 proxy season was characteristically high-consensus on routine items, with Audit and Capital proposals clearing the bar at (99% average support).

- The widest dispersion in remuneration and in a handful of board elections at complex or controlled issuers.

- In 2025, average support for the approval of the remuneration report grew by 2.68% compared to 2024. All items received above 50% support in 2025.

AGM Season Insights

Ethos Foundation activity in Switzerland generally serves as an indicator towards interesting governance related events happening in the market. During the 2025 proxy season, they were actively involved in several high-profile AGMs, consistently challenging companies on executive remuneration, governance structure, and sustainability disclosure.

At UBS, Ethos opposed the executive pay plan, a new share buyback program, and the sustainability report, citing poor climate transparency and overly leveraged variable pay. At Novartis, they rejected all remuneration items, criticizing the CHF 95 million executive package for 2026 amid a sharp rise in CEO pay. Holcim drew similar scrutiny, with Ethos opposing the chairman’s CHF 48 million pay over, 600 times the national average, and calling for greater role separation. Meanwhile, Nestlé faced opposition on discharge and sustainability votes after a water-labelling scandal, and through EEP International, Ethos mobilized 122 institutional investors to push asset managers toward ESG-aligned voting.

Across these engagements, clear patterns emerge. Ethos has adopted a firm stance against excessive, opaque, and highly variable executive pay, particularly where it risks misalignment with long-term performance. Their critiques also extend to board composition, especially the combining of CEO and chair roles, and to governance practices that appear to prioritize controlling shareholders or insiders at the expense of broader accountability. In matters of sustainability, Ethos continues to insist on transparency, third-party verification, and climate action that moves beyond box-ticking.

These interventions reflect a shift in Swiss stewardship culture. Ethos is not only holding companies accountable on a case-by-case basis but also shaping broader norms through coordinated investor action. Their strategy signals rising expectations for Swiss issuers to meet higher standards on pay fairness, governance independence, and ESG integration, backed by credible disclosure and consistent shareholder dialogue.

2026 Season Outlook

Pressure Points

Expect continued pressure on quantum and the leverage of variable pay—especially where disclosure doesn’t allow investors to assess realizable outcomes. Scenario charts and clear cap mechanisms will be key. In relation to director elections, we expect focus on board independence & discharge to intensify. Where ownership is concentrated, investors will keep using director elections (and the discharge item) to press for refresh, independence on key committees and demonstrable responsiveness.

Issuers should prioritize: for any item that draws notable opposition, provide a public, time-bound follow-up plan and report on outcomes before the next AGM.

Conclusion

Switzerland continues to post exceptionally high routine support but pay and board independence remain the pressure valves. With CEO pay trends back in the headlines, 2026 will reward issuers that prove calibration (not just state it): clearer pay design and disclosure, credible independence and refresh, and sustainability reports that stand up to binding scrutiny.

Spain

IBEX 35

Succession and AI Oversight

Introduction

Spain’s 2025 Proxy Season unfolded with few disruptions across IBEX 35 companies, signaling a period of relative stability in corporate governance.

While all proposals were approved, underlying voting trends, particularly around director elections and executive remuneration, offer a nuanced view of evolving investor expectations and proxy advisor influence.

The season was marked by high support for board nominees and a rebound in remuneration approval rates, even amid rising scrutiny.

These patterns reflect both the maturity of Spain’s governance framework and the effectiveness of company engagement strategies in navigating shareholder concerns.

Key AGM Results

- Remuneration proposals remain the most contested, despite being standard agenda items. Proxy advisor opposition rose in 2025, yet shareholder support for both remuneration reports and policies remained strong, with average approval rates increasing year-on-year.

- With average support rising to 97% in 2025. Even as ISS increased its opposition rate, no directors failed to secure majority support suggesting effective company engagement and disclosure strategies.

AGM Season Insights

Gender Parity Law and Board Impact

Spain’s Parity Law (LO/2024) mandates that listed companies achieve at least 40% female representation on their boards. This binding requirement has accelerated board refreshment efforts. Although the IBEX 35 collectively surpassed the threshold, progress remains uneven across the broader market. Boards falling short may face pressure to hasten progress ahead of the 2026 proxy season.

Board Mandates Broaden to Include AI Oversight

Spanish boards are increasingly tasked with steering AI strategy and risk oversight considering the country’s pioneering AI governance framework. Since June 2024, AESIA, the Agencia Española de Supervisión de Inteligencia Artificial, has served as Spain’s dedicated AI regulator, preparing for enforcement of the EU AI Act through the national law drafted in March 2025. Spain’s boards will likely need to integrate AI oversight into their governance framework, guided by AESIA’s regulatory regime and Spain’s transposition of the EU AI Act in March 2025.

2026 Season Outlook

Remuneration should continue to be a priority for the board with special emphasis on remuneration policy proposals because they are binding and establish remuneration direction for coming years. A few developments to keep in mind is that Glass Lewis will be using a new pay-for-performance methodology in 2026 to evaluate how executive remuneration and company performance are aligned. Both proxy advisors have signaled interest in the balance between time‑ and performance‑based equity in their policy surveys, so the results of these and any subsequent policy amendments should be considered.

Spanish boards begin preparing for AI governance and digital oversight, anticipating future EU regulation and investor interest in ethical tech deployment. We expect boards to continue operationalizing oversight: formalizing reporting lines and KPIs for AI risk, adding AI to board agendas, and forming or expanding technology, risk, or ethics committees to supervise AI programs.

Sustainability Review

Adjusting ESG Expectations

Top Trends from the 2025 European Proxy Season

The 2025 European proxy season represents a key inflection point in ESG, marked by a broad recalibration of investor expectations and corporate responses. The overall environment shifted from ambitious targets to pragmatic stewardship, with heightened emphasis on regulation-driven transparency, data integrity, nuanced shareholder engagement, and outcomes-focused sustainable investment. Five critical trends emerged across regulation, reporting, shareholder proposals, sustainable investment, and stewardship, which together have shaped the ESG landscape for European companies and investors this year.

Compliance is Key: Regulation Drive ESG Reporting

The 2025 proxy season saw significant regulatory shifts driven by the EU’s Corporate Sustainability Reporting Directive (CSRD) and the newly proposed Omnibus package aimed at simplifying and streamlining sustainability reporting. The Omnibus package notably reduces the scope of CSRD by about 80%, focusing mandatory reporting on larger companies with over 1,000 employees and higher financial thresholds. It also delays reporting requirements for many companies, providing relief by pushing back compliance deadlines for the “second wave” of companies from 2025 to 2027.

Key changes include a substantial reduction in mandatory data points and the removal of sector-specific reporting standards, aiming to ease the compliance burden without compromising transparency. The mandatory double materiality principle remains intact, requiring companies to disclose both financial impacts and broader environmental and social effects. The package also maintains a focus on climate-related disclosures aligned with the Paris Agreement and net-zero commitments.

Investors have responded by intensifying scrutiny on the quality and verifiability of disclosures, linking proxy voting to the credibility of transition plans and ESG data. Enhanced fund labeling rules are further tightening the ESG investment landscape, weeding out greenwashing and emphasizing compliance as foundational for market trust and access to capital.

These shifts mark the need for a practical recalibration, balancing ambitious sustainability goals with what is feasible for companies to accomplish, signaling that regulatory compliance is now a core strategic priority for European companies navigating the evolving ESG landscape.

Transparency Transformed: The Age of Audit-Ready ESG Data

As a result of the CSRD and associated European Sustainability Reporting Standards (ESRS), a new level of transparency in European ESG reporting has been ushered in for 2025. These regulatory frameworks demand rigorously verifiable and audit-ready sustainability disclosures, elevating transparency from narrative storytelling to a discipline of data integrity and accountability.

Corporate boards now prioritize the acquisition of high-quality, consistent, and auditable ESG data, recognizing it as foundational to meeting stringent double materiality requirements, assessing both the financial impacts of ESG risks and opportunities on their business, and their wider environmental and social effects. Formal sustainability audits have gained significant traction, often uncovering data comparability issues from prior years rather than flagging outright failures, reflecting a maturing reporting landscape.

Transparency expectations have expanded beyond climate risk disclosures to include granular metrics around diversity, governance, and supply chain emissions. Increasingly, shareholders in jurisdictions such as Spain and Switzerland are actively involved in approving these non-financial reports, underscoring a shift toward greater shareholder scrutiny and demand for substantive disclosures.

The challenge of delivering assurance-ready ESG data has catalyzed significant investment in data acquisition, analysis, and governance, with nearly half of institutional investors indicating plans to increase budgets in these areas. Meanwhile, investors express healthy skepticism toward ESG ratings alone, concerned these can incentivize reputation management rather than real impact, reinforcing the critical role of robust, traceable, and independently assured data.

Shareholder Proposals: From Volume to Value

Across the globe, environmental and social shareholder proposals faced a sharp decline in both the number filed and the levels of support. According to Diligent, overall support for environmental and social proposals dropped from 15% and 18%, respectively, in 2024 to approximately 11% in 2025, with no environmental proposals passing in major European markets for the first time. This drop reflects growing investor “proposal fatigue” and a deliberate shift to more discerning scrutiny of ESG issues rather than broad, unconditional endorsement.

Leading asset managers such as Legal & General Investment Management (LGIM) and Norges Bank Investment Management adopted refined strategies, focusing on pragmatic stewardship over prescriptive resolutions. LGIM notably voted against Equinor’s energy transition plan due to insufficient specificity and time-bound targets, demonstrating a shift to holding companies accountable for credible, climate action rather than accepting general commitments. Norges shifted from a more active role in filing emissions-focused proposals to prioritizing private dialogue and targeted stewardship that seeks measurable progress. This pivot reflects broader trends where investors are balancing strategic activism with regulatory and market complexities.

Vanguard’s 2025 European stewardship briefing also underlines this evolution. They observed that shareholder proposals increasingly require detailed, credible disclosures, challenging companies to evolve beyond broad ESG policies toward transparent metrics and robust governance. Vanguard further emphasized the growing importance of strategic dialogue off the ballot, with pre-AGM engagement playing a central role in shaping company responses.

Say-on-Climate resolutions saw relatively stable volumes compared with prior years; however, increased abstentions signaled heightened caution from passive investors balancing strategic influence with portfolio management. This careful approach aligns with BlackRock’s opening 2025 Global Voting Spotlight, which emphasizes voting decisions based on defensible, measurable outcomes rather than symbolic climate proposals. The report highlights that BlackRock supported fewer than 2% of environmental and social proposals globally, reflecting a trend toward selective backing focused on impact and integration with company strategy.

Overall, this recalibration highlights investors’ demand for ESG actions backed by data, accountability, and actionable plans, not merely aspirational targets or boilerplate policies. Shareholders now seek defensible, time-bound actions and measurable progress, sidelining generic proposals in favor of focused, feasible stewardship that drives tangible benefits.

Governance Focus and Capital Market Competitiveness

The 2025 European proxy season reflected a pronounced shift toward governance fundamentals as a primary area of investor focus. This includes intensified scrutiny on board effectiveness, director elections, executive compensation, and shareholder rights, with a view to enhancing corporate competitiveness in a rapidly evolving regulatory and economic landscape. Several markets are revising rules on meeting formats and shareholder rights to balance transparency with operational efficiency, reflecting broader competitiveness priorities across Europe.

For instance, changes in Germany require shareholder approval to renew virtual-only meeting authorizations, while Italy allows closed-door meetings until the end of 2025, impacting the platform for shareholder dialogue. Investors increasingly emphasize clear pay-for-performance in executive compensation policies and call for transparent CEO-to-median-employee pay ratios. Governance proposals received steady or increased support relative to environmental and social resolutions, signaling that governance is viewed as a foundation for sustainable, long-term value creation.

This governance recalibration intertwines with regulatory reforms aimed at strengthening Europe’s capital markets and fostering competitive yet responsible business environments. It underscores that, alongside ESG commitments, companies must elevate governance quality to attract and retain investor confidence amid dynamic proxy season pressures.

Looking Ahead

European companies face a future where ESG success demands audit-grade transparency, regulatory fluency, and demonstrable progress on climate goals. The 2025 proxy season’s recalibration marks a turning point from aspirational talk to credible action, where investor confidence hinges on data integrity, defensible transition plans, and sophisticated engagement. Forward-looking firms will embed ESG as a strategic value driver rather than compliance checkboxes.

Investor stewardship will continue to mature from passive acceptance to active, data-driven partnership, with digital tools enabling richer dialogue and governance rigor. The evolving regulatory landscape, combined with changing investor expectations, sets a high bar, rewarding transparency, accountability, and authentic ESG impact as the new normal across Europe and beyond.

Team