Industry Fund Profile – Energy Minerals

Alliance Advisors

Through the first quarter of 2025, the S&P Composite 1500 / Energy Index has reached heights only achieved twice (in 2008 and 2014), leading investors to believe that valuations of the Energy sector have pushed into over-valued territory. The S&P Energy Select Sector Index has similarly reached heights only broached twice before and so far this year, energy stocks lead all S&P 500 sectors. Understanding what has underpinned this performance helps explain the drivers of smart-money sentiment. While prices were relatively flat for all but one of the key energy products in 2025’s first quarter, only natural gas prices that have risen, rallying nearly 25%.¹ Since hitting $80 a barrel on January 15, West Texas Intermediate crude oil has fallen by nearly 30%, hitting sub $57 just recently. This scenario played nicely into the broader market sentiment that saw many factors create a “risk-off” environment, prompting a rotation out of growth-oriented sectors into more defensive and/or value-focused areas.

With this backdrop in mind, Alliance Advisors conducted shareholder analysis to see which investors were buttressing the sector’s performance. We reviewed mutual fund holdings within our innovative investor intelligence platform, Invictus®, to understand which mutual funds were the most bullish supporters of the Energy Minerals sector, and the results proved interesting. Our initial screen was for actively managed mutual funds based in the United States that have been increasing their exposure to Energy Minerals sector stocks by more than $5 million. We then filtered out any funds that did not hold at least five (5) Energy Minerals sector stocks so as to remove any anomalous outliers. When sorting this list by the percentage of purchased to owned investments, a clear trend emerged. The most bullish funds in the Energy Minerals sector were not industry funds (Oil, Gas, Commodities, etc), but rather Value focused funds followed by Global funds. Leading the list was the Allspring Large Company Value Fund managed by Ryan Brown and Harin de Silva. Underpinning the fund’s sector investment theme was a rotation into mega cap names (ConocoPhillips, EOG Resources, and Exxon Mobil) at the expense of mid- and large-cap names (Ovintiv, National Fuel Gas, and Diamondback Energy).

| Firm Name | Focus | Owned $MM | Average Owned $MM | Owned $MM Change | Owned MM Chg vs Owned | Owned % Portfolio |

|---|---|---|---|---|---|---|

| Allspring Large Company Value Fund | Value | $15,751,791 | $3,937,948 | $9,317,191 | 144.8% | 6.8% |

| Avantis US Large Cap Value Fund | Value | $40,797,877 | $2,209,713 | $13,413,305 | 49.0% | 9.9% |

| Neuberger Berman Large Cap Value Fund | Value | $852,150,066 | $207,129,403 | $193,608,892 | 29.4% | 10.3% |

| BlackRock Advantage International Fund | Global | $116,145,038 | $18,658,641 | $25,206,807 | 27.7% | 2.9% |

| Kopernik Global All Cap Fund | Global | $135,209,516 | $25,031,000 | $26,353,025 | 24.2% | 7.7% |

| Tortoise Energy Infrastructure & Income Fund | Income | $135,914,501 | $16,146,456 | $25,714,534 | 23.3% | 29.6% |

| VT III Vantagepoint International Fund | Global | $36,261,491 | $4,530,062 | $6,204,349 | 20.6% | 2.5% |

| American Funds International Growth & Income Fund | Gr. & Inc. | $611,532,032 | $143,971,314 | $92,053,634 | 17.7% | 4.1% |

| T. Rowe Price Funds SICAV - US Large Cap Value Equity Fund | Value | $64,699,823 | $13,621,709 | $9,676,773 | 17.6% | 7.8% |

| Principal Funds, Inc. - MidCap Value Fund I | Value | $84,621,157 | $6,994,692 | $9,582,887 | 12.8% | 3.6% |

Similarly, the Avantis US Large Cap Value Fund managed by Eli Salzmann and David Levine, the second largest percentage increase in the sector, was also seen rotating into meg cap sector names (Chevron, Exxon Mobil, ConocoPhillips and EOG Resources) at the expense of smaller capitalization companies (HF Sinclair, PBF Energy, Civitas Resources, SM Energy, and APA Corporation). Helping Chevron during this period was the US President weighing a plan to extend Chevron’s license to pump oil in Venezuela, as per Reuters.

The Neuberger Berman Large Cap Value Fund, the third largest increase with a dedicated value focus, seemed to apply a comparable approach by heavily increasing exposure to EOG Resources and Chevron, though instead of sourcing capital from smaller market capitalization companies chose to rotate within the mega cap space by reducing exposure to Exxon Mobil and Phillips 66. In the fund’s April commentary, fund manager David Levine wrote, “From a sector allocation standpoint, the Fund benefited from an overweight positioning in energy and an underweight positioning in information technology».

In shifting to the Global funds, the most bullish fund was the BlackRock Advantage International Fund managed by Raffaele Savi, Kevin Franklin and Richard Mathieson. This fund mirrored the earlier trends of increasing exposure to mega cap names, though those outside of the United States (Shell PLC, Equinor ASA, and TotalEnergies SE), each within the Integrated Oil industry. When highlighting the contributing factors to performance, the fund’s most recently commentary stated,

Fundamental quality measures focused on sustainability of earnings and penalizing companies with high wage pressures were the top contributors… Collectively, stock selection was strong across Europe through a preference for domestic financials and defense stocks over those reliant on global trade.

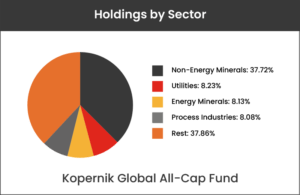

Another globally-focused fund exhibiting bullish sentiment in the Energy Minerals sector was the Kopernik Global All Cap Fund managed by Alissa Corcoran and Dave Iben. This fund made a rotation into North America with its three largest purchases in Canada’s MEG Energy, US-based Expand Energy and Range Resources. This trend follows in line with the fund’s driving principle that being an opportunistic portfolio will have a low correlation to other managers. The fund’s primary philosophy and process is designed to capitalize on market dislocations based on fear and greed.

Another globally-focused fund exhibiting bullish sentiment in the Energy Minerals sector was the Kopernik Global All Cap Fund managed by Alissa Corcoran and Dave Iben. This fund made a rotation into North America with its three largest purchases in Canada’s MEG Energy, US-based Expand Energy and Range Resources. This trend follows in line with the fund’s driving principle that being an opportunistic portfolio will have a low correlation to other managers. The fund’s primary philosophy and process is designed to capitalize on market dislocations based on fear and greed.

The period for which these holdings analysis encompassed was historically unique, as the overarching influence on investor sentiment was the US President’s ever-changing tariff strategy. Crude benchmarks suffered from demand concerns related to these tariff concerns. After providing initial headwinds, a decision to pause tariffs on non-retaliatory nations for 90 days and lowered reciprocal tariffs to 10% provided some tailwinds. Also, tanker data had Russian, Iranian and Venezuelan crude exports all rebounding in March, despite US sanction threats.

For corporates looking to influence their shareholder constituents, Alliance’s team of market experts can help you understand shifting market dynamics to ensure your time is spent with the “right” shareholders instead of the traditional peer-focused investors.

¹ Energy Information Administration

![]()

If you would like to receive our regular blog featuring reports, news and reviews in future, please enter your details in the form below.