Overview

Although not without challenges, the 2024 U.S. Proxy Season Review produced largely positive outcomes for U.S. corporations. Issuers achieved better results on their executive compensation programs than in 2023 and defeated all but a handful of environmental and social (E&S) initiatives. Even in two of the year’s testiest annual meetings—Exxon Mobil and Tesla–investor votes underscored that earning strong—and certainly exceptional—financial returns dwarfed all other controversies.

Get your copy of the full report.

Some of the notable developments that arose this spring were the following:

Governance proposals outperformed: Resolutions on traditional governance topics outdid the results of all other categories of shareholder proposals, accounting for 42 of this season’s 45 majority votes, which in 14 cases were unopposed by the boards. Thirty-one of the successful proposals sought the removal of supermajority voting provisions in favor of a simple majority, which holds near universal appeal for shareholders.

E&S proposals skid further: E&S initiatives suffered their third year of diminishing average support, even when factoring out those from conservative-leaning proponents (“anti-ESG”) and despite consistent levels of support from proxy advisors Institutional Shareholder Services (ISS) and Glass Lewis year over year. Only three resolutions accrued majority votes, compared to seven last year: two on reducing greenhouse gas (GHG) emissions and one on lobbying disclosure. The slippage in results reflects the views of some major asset managers that many of the E&S resolutions reaching ballots are overly prescriptive, poorly targeted or lacking economic merit.

ESG under siege on multiple fronts: Aside from slackening investor support for their resollutions, environmental, social and governance (ESG) activists are grappling with companies tempering their climate commitments and paring back their DEI programs. This season they encountered a new challenge—namely, a greater willingness by some firms, such as Exxon Mobil, to fight back against perceived abuse of the shareholder proposal process. For their part, conservative groups ramped up their proposals countering ESG measures though these still drew only meager support from institutional investors. Meanwhile, the broader debate over ESG continues to play out via litigation, state actions, and Congressional hearings.

Unions flexed their muscles: Sparked by last year’s large-scale strikes, organized labor was more active this season. Union pension plans not only stepped up their volume of shareholder proposals, but also took their activism to a new level by launching their first-ever proxy contest at Starbucks. Although the fight was withdrawn, it signals a new tactic that trade unions could deploy at other companies facing labor disputes.

Artificial intelligence (AI) excelled among new campaigns: Shareholder activists undertook a variety of new initiatives this season involving stricter director resignation and renomination policies, a “say on director pay,” biodiversity impact assessments, and paying workers a living wage. While most attracted very limited investor interest, several calling for AI transparency reports received a remarkable level of first-time support, reaching as high as 43.3%.

Executive compensation improved: Investor approval of management say-on-pay (SOP) proposals this season outpaced the first half of 2023 with an average vote of 91% across all U.S. public companies and a failure rate of only 1.3%. The improved results reflect a lower incidence of adverse recommendations from ISS, as well as effective engagement between issuers and investors.

Regulations in flux: The regulatory landscape is rapidly evolving towards one that looks more favorable to businesses. The SEC has delayed much of its 2024 rulemaking activity until after the fall elections and paused its climate change disclosure rule while courts work through legal challenges. A recent federal court ruling may also force the Commission to reinstate key provisions of the proxy advisor rule. And in a blow to the administrative state, the U.S. Supreme Court (SCOTUS) ended its 2024 session with a series of landmark decisions that will make it easier to challenge a wide range of federal regulations.

This report examines some of the predominant themes, vote results and trends at all U.S. public company annual meetings during the first half of 2024. Note that shareholder proposal votes are based on “for” and “against” votes and exclude abstentions. The number of shareholder proposal submissions are estimates based on SEC filings, proponent websites and media reports. Proxy advisor recommendations are derived from ISS Voting Analytics and Diligent Market Intelligence.

Activists Set the Tone for 2024 and Beyond

Proposal Volume Swells

This season, shareholder activists kept up the pressure on ESG issues, filing an estimated 990 resolutions through June. Based on proxy statements being filed for fall annual meetings, the year-end figure will easily surpass the 995 submissions for all of 2023.

Consistent with previous years, corporate gadflies John Chevedden, Kenneth Steiner, James McRitchie and Myra Young (the “Chevedden group”) accounted for about one-third of all shareholder resolutions filed. These included over half of the governance proposals, nearly two-thirds of the compensation-related proposals and 10% of the E&S proposals, up from 6% last year due to their increased sponsorship of political activity resolutions.

Labor union pension plans nearly doubled their volume of filings, accounting for 10% of the total 2024 submissions, compared to 5% last year, largely due to a new initiative by the United Brotherhood of Carpenters and Joiners of America (UBC) on director resignation policies. Their other topics of interest included unionization rights, worker safety, and the labor impact of artificial intelligence and companies’ climate strategies.

Conservative-oriented proponents also increased their proposal activity, particularly in the E&S space. This year, they sponsored 12% of all proposal filings (versus 10% in 2023), including 18% of E&S filings (versus 15% in 2023). In addition to boosting their submissions on decarbonization risks, they focused heavily on workforce civil liberties and politicized debanking.

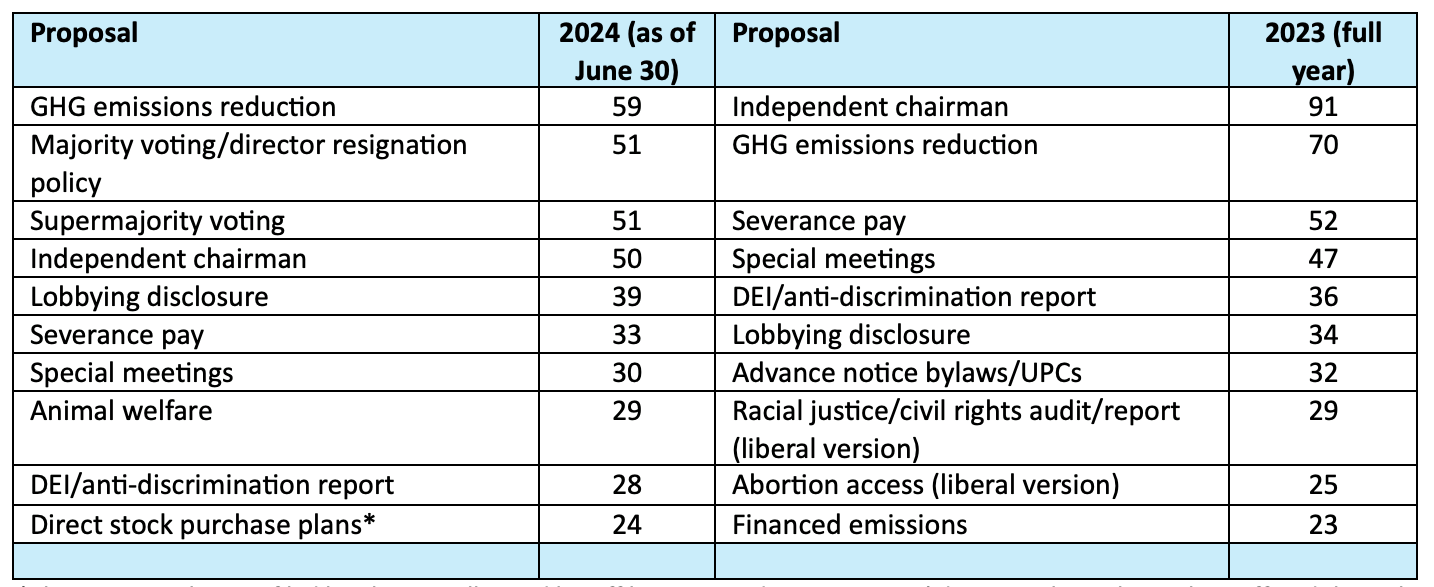

Shifting Priorities

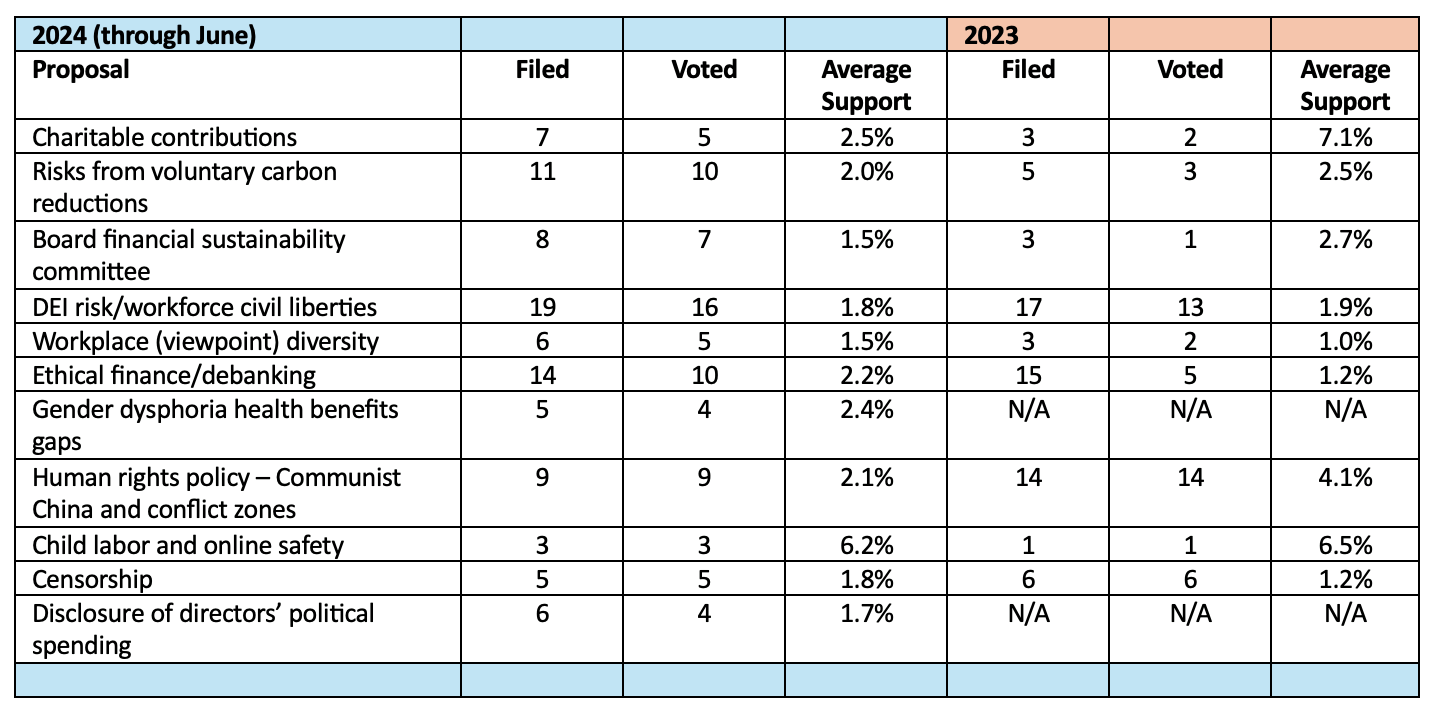

As reflected in Table 1, shareholder activists repositioned their main areas of focus from last year. Animal rights groups—joined this year by The Accountability Board—continued to scale up their proposals on farm animal welfare following Carl Icahn’s 2022 proxy fight at McDonald’s over its treatment of pregnant sows.

Table 1: Top Ten Shareholder Proposal Filings: 2024 – 2023

*These proposals were filed by Chris Mueller and his affiliates regarding companies’ direct stock purchase plans offered through their transfer agent, Computershare. All were omitted as ordinary business or for technical deficiencies, other than two pending for fall annual meetings.

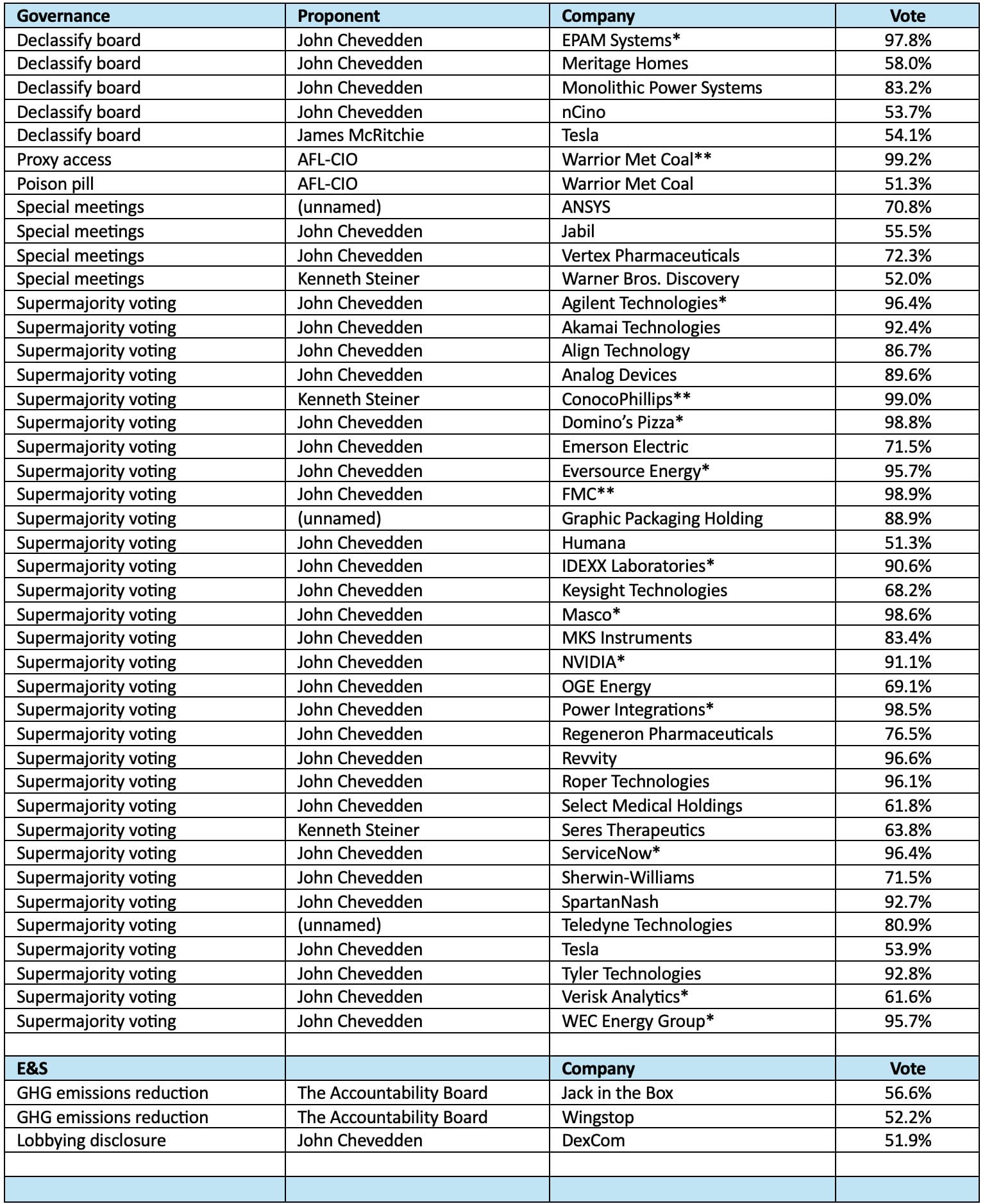

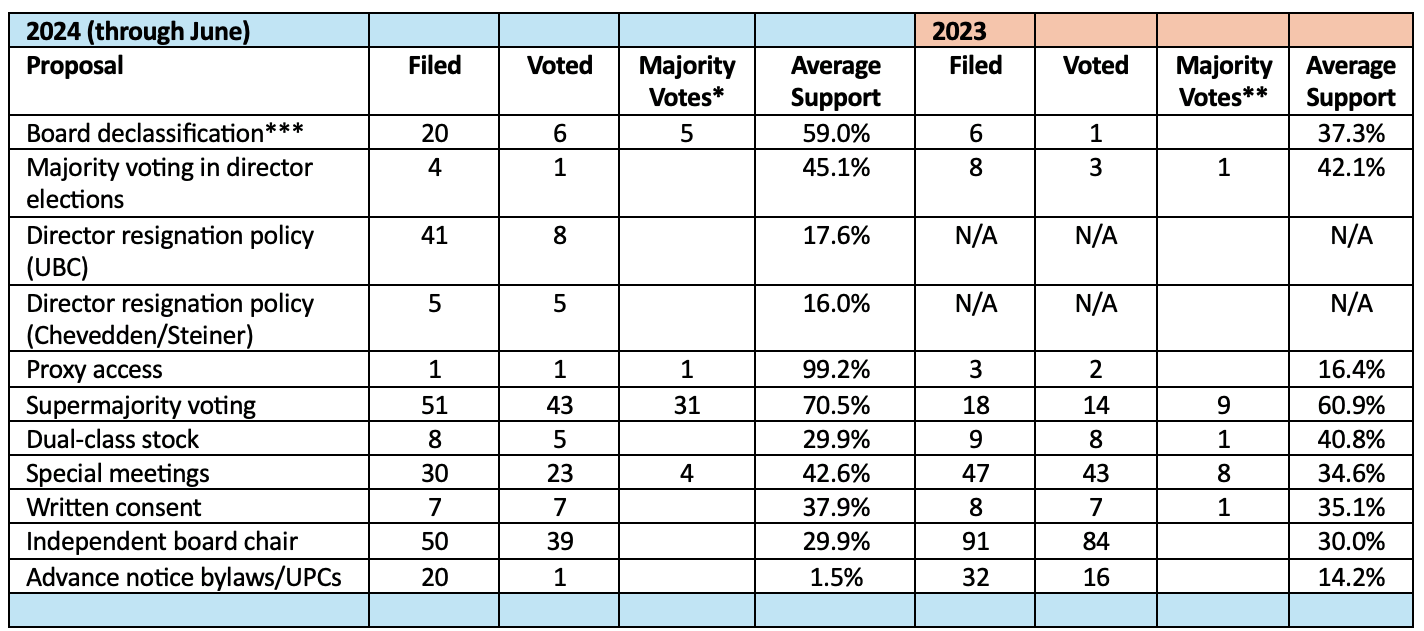

Chevedden and Steiner pulled back from two of their top 2023 initiatives: independent board chairs, where average support has hovered around 30% since 2022, and executive severance pay, which they began in earnest two years ago, but support levels have since dropped off. Instead, they redirected their efforts towards a more widely accepted measure, namely, the repeal of supermajority voting provisions, which yielded the most majority votes of all 2024 shareholder resolutions (see Table 2).

Table 2: 2024 Shareholder Proposal Majority Votes (through June)

*The board made no recommendation on the proposal

**The board supported the proposal.

Other shareholder activists similarly backed off from some of last year’s headline issues. After being popularized in the aftermath of George Floyd’s death, calls for racial equity and civil rights audits substantially diminished amid waning support levels. Proposals dealing with reproductive healthcare, which first appeared on a small scale in 2022, also declined from their high point last year when ISS switched from supporting to opposing them.

McRitchie and Young likewise tempered their campaign on fair director elections, which they began last year in response to some abusive practices, such as onerous advance notice and disclosure requirements, following the introduction of universal proxy cards (UPCs). They ultimately withdrew most of their 2024 resolutions after companies agreed to amend their governance guidelines to stipulate that the board’s determination of a shareholder nominee’s eligibility would be based on the requirements of Rule 14a-19, applicable law and the company’s bylaws and not on their suitability to serve on the board.

More Omissions, Fewer Withdrawals

According to SEC staff, the volume of no-action requests through April 2 was up about 50% compared to the 2022-2023 season and up by 13% compared to the 2021-2022 season. Excluding withdrawn proposals, the staff granted 64% of requests, compared to 58% last year1.

The uptick in omissions primarily centered around certain governance and compensation-related proposals that were newly introduced this year, as opposed to E&S resolutions where the level of exclusions (8% of submissions) was on par with 2023. Among these were the UBC proposals on director resignation policies and binding bylaw resolutions by Chevedden to hold a “say on director pay,” which were successfully challenged as violations of state law. A slew of proposals from a group of individual investors on companies’ direct stock purchase plans were nixed as ordinary business or for procedural defects.

The proportion of shareholder resolutions reported as withdrawn was down slightly from 2023 due to fewer compromises reached on E&S resolutions where the withdrawal rate was 24% compared to 27% last year. In both years, the E&S proposals most frequently withdrawn pertained to reducing GHG emissions and diversity, equity and inclusion (DEI) reporting.

Asset Managers in the Crossfire

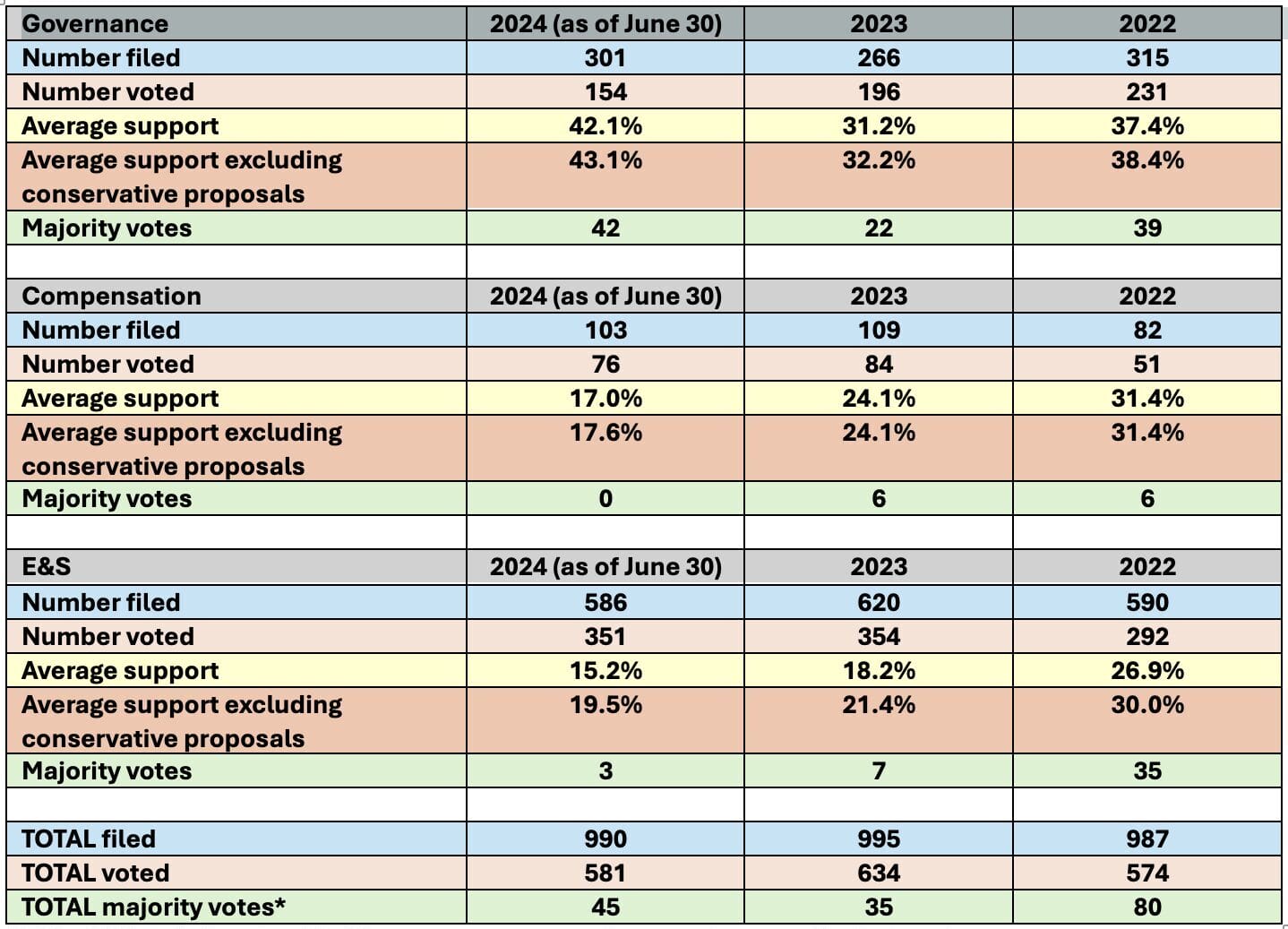

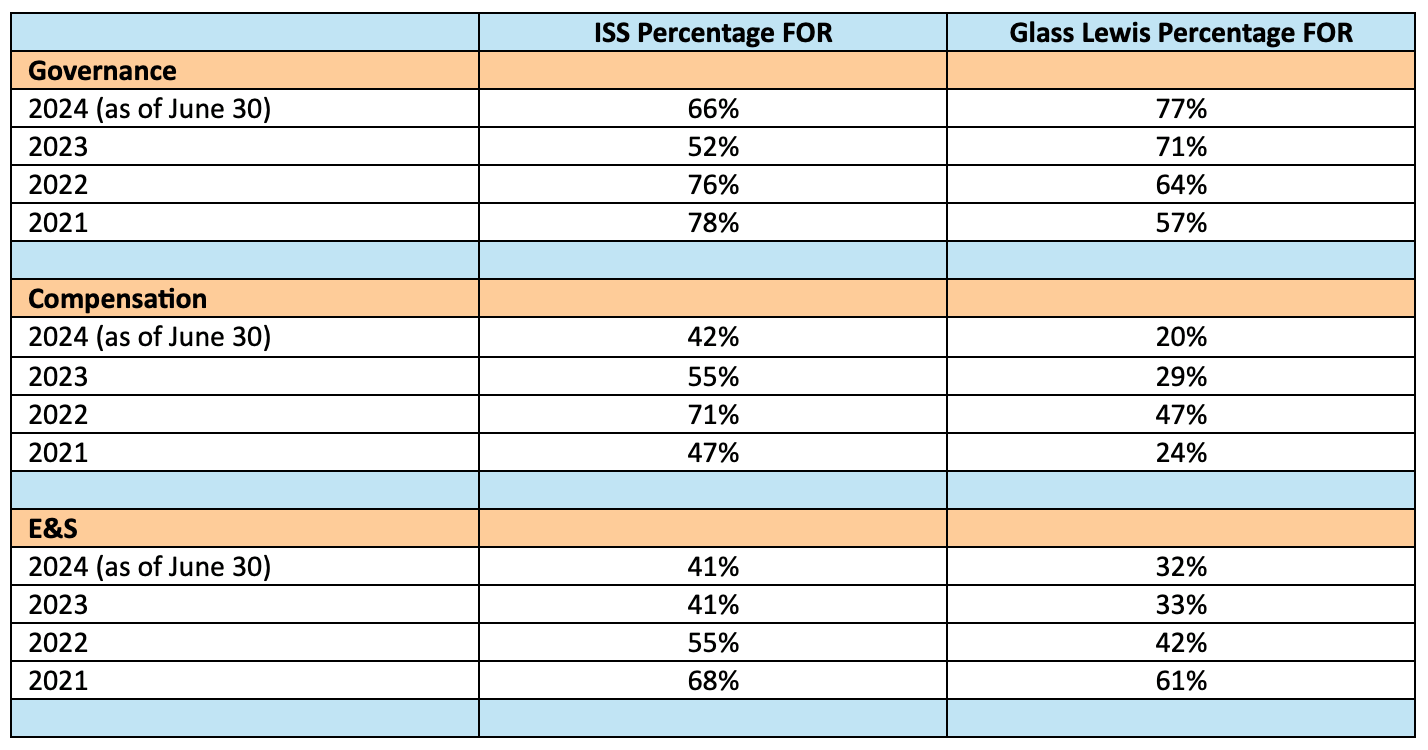

Average support for E&S proposals continued the downward slide that began two years ago, even when excluding those from conservative proponents (see Table 3). Following the SEC’s 2021 guidance (Staff Legal Bulletin No. 14L), a higher number of E&S proposals have reached ballots on the basis that they have a broad societal impact. However, a number of major asset managers have deemed many of them to be of poor quality–overreaching, redundant or lacking economic merit–and explicitly called out these shortcomings in their 2024 voting policy updates and quarterly stewardship reports2. Proxy advisor support for E&S resolutions has also fallen over this period but was consistent between 2023 and 2024 (see Table 4).

Table 3: Shareholder Proposal Voting Trends

*Of the 2024 majority votes, 14 of the governance proposals were not opposed by the board.

Of the 2023 majority votes, five of the governance proposals and one of the E&S proposals were not opposed by the board.

Of the 2022 majority votes, 13 of the governance proposals and seven of the E&S proposals were not opposed by the board.

Table 4: ISS and Glass Lewis Support for Shareholder Proposals

Compounding this voting behavior is the heightened scrutiny large asset managers are facing from GOP lawmakers and state officials over their ESG investment activities. This has spurred their moves to create proxy voting choice options for their clients and to depart from climate alliances, such as Climate Action 100+ and Net Zero Asset Managers Initiative, in favor of conducting their engagements independently.

One firm -JPMorgan Asset Management, is also distancing itself from the influence of the proxy advisory firms3.

Because of their restrained support for E&S proposals, asset managers were themselves more frequent targets of shareholder activists this year. A coalition of non-profit groups and sustainable investment firms filed resolutions at BlackRock, State Street, JPMorgan Chase and Goldman Sachs Group to address misalignments between their public commitments to diversity and climate change and their 2023 proxy voting records and voting policies. The Sierra Club separately asked BlackRock and State Street to report on how they could use their stewardship to effectuate real-world decarbonization. In all, these initiatives mustered only 8.1% support on average.

Recognizing the pro- and anti-ESG controversies surrounding proxy votes, McRitchie took a different approach and urged nine financial institutions to ascertain their clients’ voting preferences and values and consider offering them more granular proxy voting options. This idea attracted only 6% support in the sole vote at Northern Trust.

BlackRock also came under fire from U.K.-based activist Bluebell Capital Partners for being inconsistent in implementing its ESG strategy, including continuing its investments in fossil fuels. Bluebell proposed a bylaw amendment to require that the board chair be an independent director, which would have removed co-founder and CEO Larry Fink from his chairmanship. The resolution garnered only 13.1% support—the lowest vote among all of this year’s independent chair proposals—and was opposed by the proxy advisors because its binding nature would constrict the board’s flexibility with respect to its leadership.

Companies Fight Back

Corporate pushback against the deluge of shareholder proposals in recent years was also more pronounced this season. Frustrated with facing recurring resolutions, Amazon.com and Exxon Mobil were more vocal about calling out abuse of the shareholder proposal process by ESG activists.

In a preface to the 14 shareholder proposals presented in its 2024 proxy statement, Amazon lambasted the serial resolutions it receives from a large but growing subset of investors that raise societal concerns that have little or nothing to do with the company’s business or with investors’ or fiduciaries’ goal of enhancing the value of their investments. Amazon has received more than 20 shareholder proposals in each of the past five years and more than 160 in the last decade.

Exxon Mobil took the bolder step of sidestepping the SEC no-action process in favor of a judicial determination on the omission of a repeat proposal by Arjuna Capital and Follow This to accelerate the pace of its GHG emissions reduction, including those of its customers (Scope 3). Exxon argued that under the proxy rules the proposal was excludable as ordinary business because it would force the company to drastically shrink its core business operations. The resolution also did not meet the resubmission threshold for previously defeated proposals.

Ultimately, Exxon’s complaint was dismissed on procedural grounds because the proponents withdrew the resolution and Arjuna pledged not to submit, or work with others to submit, any GHG or climate change proposals at Exxon in the future. Beyond blocking the 2024 proposal, Exxon’s larger objective was to seek clarity from the U.S. district court on what violates Rule 14a-8 in view of the SEC’s more restrictive standards in recent years for excluding ESG proposals. The matter is undergoing another judicial review by the Fifth Circuit Court of Appeals in National Center for Public Policy Research v. SEC.

It remains to be seen if other companies will follow Exxon’s lead and take a “direct-to-court” approach to keep shareholder resolutions off their proxy ballots. Although Exxon’s lawsuit panicked some investors over its potential chilling effect on ESG efforts, the fallout to Exxon was minimal, particularly in view of its stellar financial performance. The board was overwhelmingly reelected with an average of 95% support.

Environmental Issues

GHG Emissions

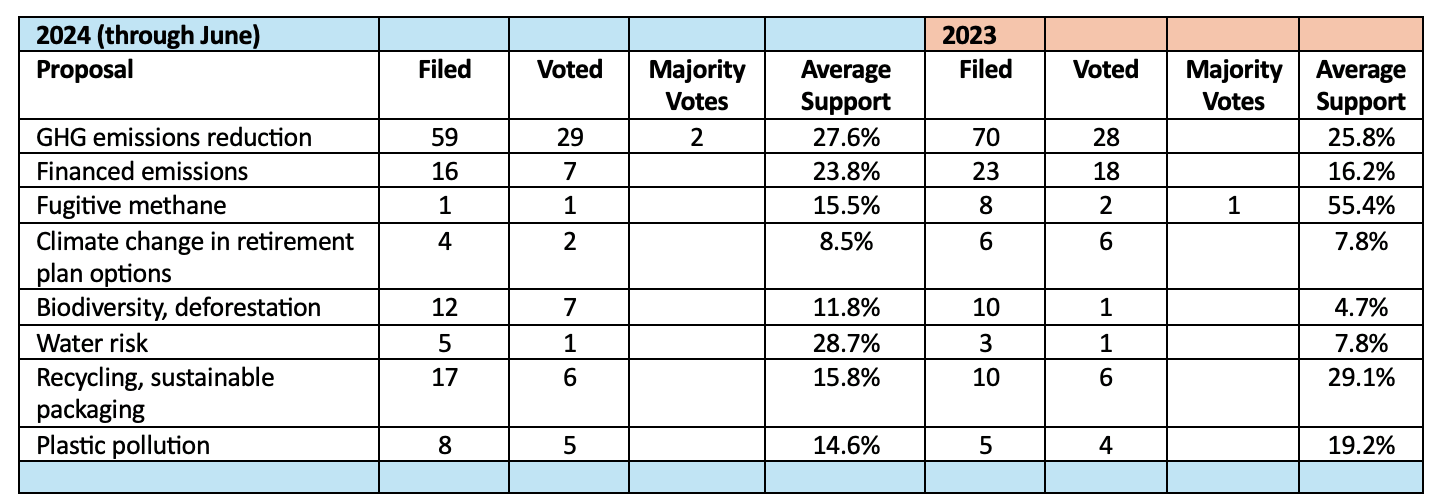

Investor support for proposals to reduce GHG emissions has declined dramatically since 2021, even as the number of submissions has escalated and proportionately more went to a vote. Three years ago, 20 resolutions were filed and all five voted received majority support, with an average of 72.6%. In the first half of 2024, 29 of the 59 submissions went to a vote, generating two majorities and an average of 27.6%.

Proponents attribute this trend to the expansion of targets beyond the largest corporate emitters to other sectors and small-cap firms where investors may have questioned the relevance of climate action. However, the specificity of the demands has also increased due to the SEC’s more permissive stance on proposals that suggest specific targets, timelines, methods or details for a report or action.

This year’s proposals generally called for the adoption of interim and long-term science-based GHG emissions reduction targets across the full value chain in alignment with the Paris Accord goals. The highest votes were achieved at Jack in the Box (56.6%), Wingstop (52.2%), and Denny’s (49.9%), all of which were sponsored by The Accountability Board, which focuses on the food industry. Two proposals remain pending for the second half of the year at Constellation Brands and Casey’s General Stores.

At least 19 proposals were withdrawn (32%), considerably below last year’s withdrawal rate (49%). Several granular proposal variations were omitted as micromanagement, including the Green Century Funds’ request for a breakdown of GHG emissions by product category and As You Sow’s request that GHG reduction targets not include the use of carbon offsets and avoided emissions.

Financed Emissions

Shareholder proponents restructured their 2024 proposals on climate-related finance after some of last year’s versions were regarded as too extreme, pulling down the voting average to 16.2%. These included the adoption of a no fossil fuel expansion policy and setting absolute 2030 GHG reduction targets for oil, gas and power sector lending and underwriting.

The latest idea on this front, proposed by the New York City Public Retirement Systems, called on five large banks to disclose their clean energy supply financing ratio, which would show what proportion of their total financing goes to low carbon energy versus fossil fuel projects. Citigroup and JPMorgan Chase agreed to the disclosure while support at three other financial institutions averaged 25.9%.

A new initiative by As You Sow asked six major banks to report the proportion of emissions in their highest emitting portfolio sectors that were attributable to clients that are not aligned with a credible net-zero pathway. All of the banks have committed to net-zero financed emissions by 2050 and have published interim (2030) targets for reducing emissions in their auto manufacturing, oil and gas, and power generation sectors. Although none of the proposals reached ballots due to micromanagement exclusions, a withdrawal was clinched at Citigroup after it released a report addressing the climate transition progress of its energy and power clients.

As You Sow had more success with a repeat proposal at several big insurers to report on how they plan to measure and reduce GHG emissions from their financing, underwriting and investment activities. The resolutions averaged 25.7% support, up from 18.8% in 2023.

Biodiversity

Company impacts on biodiversity and nature loss is an emerging issue for investors following last year’s release of final recommendations by the Task Force for Nature-Related Financial Disclosures (TNFD). Five resolutions were filed this season asking for a material biodiversity dependency and impact assessment in line with the TNFD framework. Three were withdrawn due to company commitments and the two voted received 16.1% at Home Depot and 18.4% at PepsiCo. Notably, in 2022 Home Depot received a majority vote on a related proposal to report on its efforts to eliminate deforestation in its supply chains.

As You Sow separately filed a first-time resolution at auto manufacturers calling for a moratorium on the use of deep sea-mined minerals in electric vehicle batteries, which can cause habitat and ecosystem loss. These received 12.6% at General Motors and 7.7% at Tesla.

Plastics and Recycling

As You Sow and Green Century continued their ongoing campaign to reduce environmental harm to oceans and waterways from plastic pollution. Most of their efforts were directed at retail, restaurant, hotel and consumer goods companies to shift from single-use plastics to sustainable packaging. Compared to last year, a much higher proportion of these resolutions were withdrawn (over half) due to company commitments, while the six voted received lower support on average—15.8% versus 29.1% in 2023.

The proponents also reintroduced proposals at petrochemical companies to shift from virgin plastic to recycled polymer production or, alternatively, to report on the financial implications of reduced demand for virgin plastic. These resolutions averaged 14.6%, down from 19.2% last year.

A new focus area this year was how clothing manufacturers could reduce water pollution from the plastic microfibers in their textile products. As You Sow and Green Century reached agreements with all three targets (lululemon athletica, NIKE and VF). Meanwhile, faith-based investors reoriented some of their tobacco proposals from health risks to tobacco product waste, specifically microplastics from cigarette filters. These received little traction, garnering 8.5% at Altria Group and 6% at Walgreens Boots Alliance.

Key Environmental Proposals (excluding conservative versions)

Labor Issues

Organized labor groups were highly active this year, prompted by major strikes and protracted labor disputes in 2023. In addition to increasing their submissions of proxy proposals, they co-opted the tactics of traditional activists.

The Strategic Organizing Center union coalition launched a first-time proxy fight by a special interest group, nominating three labor-affiliated representatives to the Starbucks board. The dissidents ultimately withdrew after the two sides agreed to work towards a foundational framework on collective bargaining.

The American Federation of Labor & Congress of Industrial Organizations (AFL-CIO) and its affiliate the United Mine Workers of America made use of Rule 14a-4(c) to conduct their own proxy solicitation for a package of governance reforms at Warrior Met Coal, which won them two majority votes: to seek shareholder ratification of any future poison pill and to adopt a market-standard proxy access bylaw, which was supported by the board. Notably, this was the only proxy access measure on 2024 ballots.

Organizing Rights

Proposals to uphold the internationally recognized rights of freedom of association and collective bargaining were a primary thrust of union pension plans this year. Nearly the same number were filed (15) and voted (10) as last year, but average support declined to 25.7% from 33.1% in 2023 when a proposal received a majority vote at Starbucks.

A new type of resolution filed by the SOC Investment Group at Delta Air Lines was omitted as micromanagement. It asked the company to disclose to disclose “labor suppression” expenditures that are intended or could be viewed as intending to dissuade employees from joining or supporting a union.

Worker Safety

Proposals on worker safety more than doubled in volume this year as a result of AFL-CIO campaigns at railroad companies following the East Palestine derailment and at wireless carriers due to deaths and injuries to cell tower technicians. The resolutions sought the adoption of a board safety committee or a third-party safety assessment.

Average support receded to 15.3% due to low support levels on the railroad safety committee proposals (6.2% on average). Last year’s 34% average (excluding a floor proposal) was bolstered by a majority vote at Dollar General over workplace safety violations assessed by the Occupational Safety and Health Administration.

Just Transition

For a third year, the International Brotherhood of Teamsters, United Steelworkers and like-minded social activists asked companies to report on how they plan to address the impact of their climate change strategies on employees, supply chain workers and communities of operation in line with the International Labor Organization’s “just transition” guidelines.

Out of nearly a dozen filings, the proponents extracted commitments from four companies and the five proposals voted yielded 20.8% average support, down from 23.7% in 2023. The highest vote recorded this year (40.4%) occurred at Ryder System.

Artificial Intelligence

The rapid growth of generative AI in business has brought about a multitude of concerns over intellectual property rights, customer privacy, labor dislocations resulting from automation, and the dissemination of misinformation and disinformation.

This year, the AFL-CIO and other pension plans spearheaded nearly a dozen proposals dealing with the workforce and human rights impacts of AI. Prompted by last year’s labor disputes between creative unions and Hollywood studios, entertainment and Big Tech companies were asked to report on whether they had adopted any ethical guidelines to protect workers, customers and the public from harms related to the use of AI. This initiative averaged 26.8% support and scored remarkably high votes at Apple (37.5%) and Netflix (43.3%).

Less popular were resolutions calling for the establishment of a board committee tasked with AI oversight, which received 7.4% at Alphabet and 9.7% at Amazon. According to a report by Orrick, only 9% of S&P 500 companies have disclosed the role of the board or committees in overseeing AI-related risks, which most often was assigned to the full board or the audit committee4.

As in 2023, AI factored into human rights resolutions which called for an assessment of the user privacy risks of AI-driven targeted advertising or of the risk that AI would amplify misinformation and disinformation. The proposals averaged 16.6% and 17.2%, respectively, and may have passed were it not for the targeted companies’ (Alphabet and Meta Platforms) unequal voting structures.

Coming up in the fall, As You Sow is introducing a new proposal at Microsoft with a tie-in between AI and climate change—namely, to report on the risks of providing advanced technology, such as AI and machine learning tools, to facilitate new oil and gas production. A related issue, which has yet to be raised by shareholder activists, is the build-out of data centers to support AI workloads which consume massive amounts of electricity. In their recent sustainability reports, Alphabet and Microsoft acknowledged that their GHG emissions grew significantly over the last four to five years due to their data center energy consumption.

Key Labor Proposals

Other Social Issues

Diversity and Anti-Discrimination

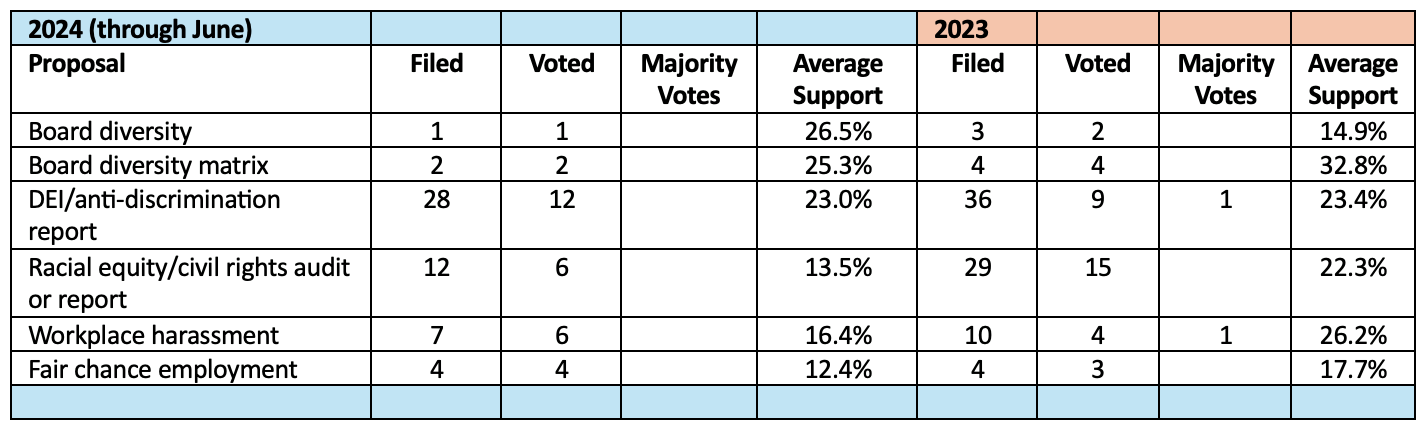

As in 2023, one of the most prevalent shareholder proposal topics this year–largely sponsored by As You Sow–asked for reports on the effectiveness of companies’ DEI and anti-discrimination efforts. While the volume of filings declined to 28 from 36 last year, the proportion going to a vote increased due to fewer settlements. This year, only 50% of the proposals were withdrawn, compared to 67% in 2023, usually by the company agreeing to disclose EEO-1 form data on hiring, retention and promotion rates. Those voted elicited a comparable level of support as last year, averaging 23%.

Requests for racial equity and civil rights audits have been on the decline from their peak in 2022. This year only 12 proposals were submitted, compared to 29 in 2023 and 48 in 2022. Average support plunged to 13.5% this year, from 22.3% in 2023 and 44.9% in 2022.

Going forward, last year’s SCOTUS decision to strike down affirmative action in college admissions will continue to have a chilling effect on companies’ diversity initiatives. Due to the growing risks of lawsuits, EEOC complaints and customer boycotts, a number of firms have altered their public communications around DEI, cut back on DEI staff and removed or de-emphasized DEI metrics in executive incentive plans5. In June, Tractor Supply became the latest high-profile DEI casualty which, amid consumer backlash, announced that it was eliminating its DEI roles and retiring both its DEI and carbon emissions goals. It will additionally cease sponsoring non-business activities, such as Pride festivals and voting campaigns, and will no longer submit data to the Human Rights Campaign.

Key Diversity and Anti-Discrimination Proposals (excluding conservative versions)

Political Influence

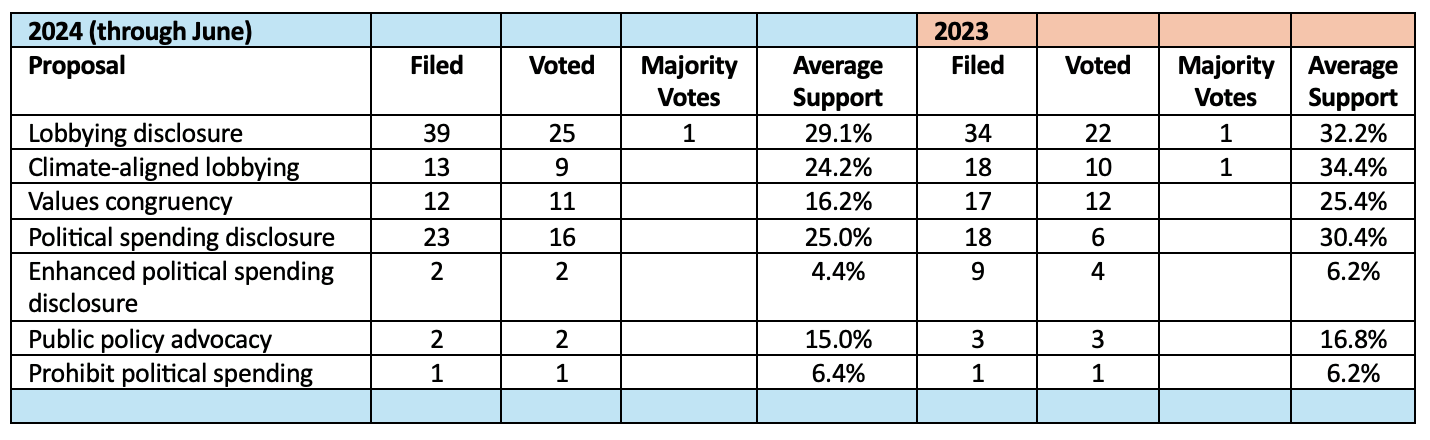

Despite being an election year, the volume of filings on political activities—including those sponsored by conservative proponents–fell 18% from last year. Average support also dropped year over year on every proposal type, other than a repeat resolution asking Verizon Communications to discontinue its political and electioneering spending, which remained essentially flat at 6.4%. The single majority vote was on lobbying disclosure at DexCom (51.9%).

This year, the Chevedden Group was the most prolific filer, sponsoring nearly two-thirds of the political spending and lobbying disclosure proposals (versus 35% last year) and 31% of the resolutions on climate-aligned lobbying (versus 17% last year). Over one-third of the lobbying proposals were resubmissions which had previously earned strong support. This year, votes on lobbying resolutions averaged 29.1%, down from 32.2% in 2023. All but a few of the election spending proposals were at new targets which scored poorly on the Center for Political Accountability’s CPA-Zicklin Index6. These generated 25% support, down from 30.4% in 2023.

Last year, CPA affiliates began promoting its Model Code calling for enhanced political spending disclosure—namely, disclosure of third-party recipients of company donations and the amount they spend on political activities. Only two were introduced this year–at Delta Air Lines and Elevance Health—which averaged 4.4% support, compared to 6.2% in 2023.

Key Political Influence Proposals (excluding conservative versions)

Healthcare

For a fourth year, faith-based investors continued to press Big Pharma over the affordability of prescription drugs. This season, they moved off their advocacy around COVID therapeutics and vaccines and focused on the impact of patent exclusivities on patient access to medicine. The six proposals filed were repeats from last year, of which four were withdrawn and two received an average of 17% support, down from 20.4% in 2023.

The proponents also took a human rights approach to the issue by asking three major drugmakers to adopt a code of conduct or undertake a human rights impact assessment regarding the human right to health, including access to essential medicines. Withdrawals were negotiated with two companies, while the sole vote at Eli Lilly received 10% support.

Healthcare access proposals expanded this year to cover not only abortions but also abortion pills and gender-affirming care7. They generally asked how companies are addressing data privacy concerns or the impact on employees of state laws restricting these products and services. A new proposal also emerged at Alphabet on how it is reducing the dissemination of misleading content on its platform relating to reproductive care, such as crisis pregnancy centers that do not provide abortions. This was the only abortion-focused resolution that Glass Lewis supported this year. ISS opposed all of them, which has been its practice since 2023. In all, 11 proposals were filed – less than half the volume of 2023 – and the six voted averaged 8.6% support, below last year’s average of 11.1%.

The New York State Common Retirement Fund (NYSCRF) concentrated on maternal morbidity with a resolution at HCA Healthcare to report on how it can improve healthcare outcomes, particularly for racial and ethnic minorities. It withdrew similar proposals last year at three other healthcare companies, while this year’s vote garnered 8.5% support. Along these lines, Mercy Investment Services reworked its racial equity audit proposal at UnitedHealth Group—which was withdrawn—to focus on racial and ethnic healthcare disparities.

Key Healthcare Proposals (excluding conservative versions)

Human Rights

Resolutions on corporate human rights policies covered familiar topics and were light in number compared to other types of social proposals sponsored by ESG activists. Average support on many issues held steady at 2023 levels.

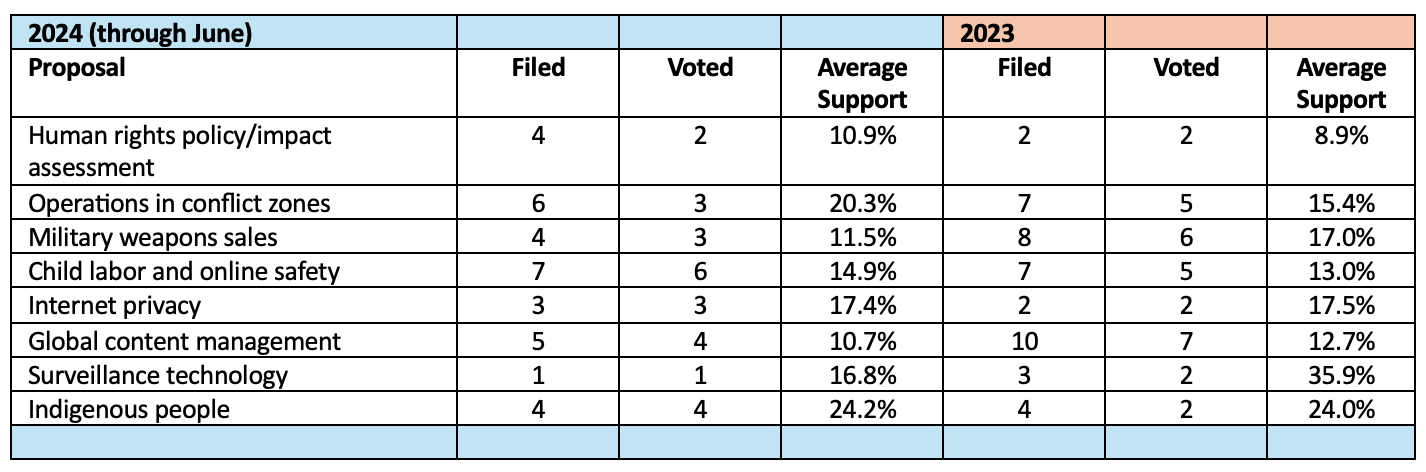

Since last year, the war in Ukraine has sparked an interest in weapons sales and company operations in conflict-affected and high-risk areas (CAHRA). These included reporting on the human rights risks and impacts associated with the sale of defense products and dual-use items, such as semiconductor chips, used in weapons systems. Other than Analog Devices, where the resolution was withdrawn, all were at repeat targets where support averaged 11.5%, down from 17% in 2023. Proposals dealing with operations in CAHRA and countries with human rights abuses received stronger support, averaging 20.3% compared to 15.4% last year. By volume, these were surpassed by resolutions from conservative proponents addressing companies’ business activities in war zones or ties to oppressive regimes, particularly Communist China. However, the voting results were vastly lower, in the single-digits (see next section).

Child exploitation and online safety was also a common concern for both liberal and conservative investors. Religious groups and social responsibility funds filed proposals at several food and apparel companies to evaluate and address child and other forced labor practices throughout their value chains. They also asked Alphabet, Apple and, for a fifth time, Meta Platforms how they were reducing harms to children using their digital media platforms, such as sexual exploitation, cyberbullying, and mental health impacts. In all, average support moved up to 14.9% from 13% last year, while the proposal at Apple was withdrawn. Conservative versions of the proposals (addressed in the next section) averaged only 6.2%.

For a third year, mostly faith-based organizations questioned large banks and insurers about the impact of their oil and gas project financing and underwriting on indigenous people. Both the number of filings (four) and average support (24.2%) were comparable to 2023.

Other common types of human rights proposals, such as those dealing with surveillance technology, internet data privacy, and content moderation by media outlets, probed more specifically this year into the impact of generative AI and the dissemination of misinformation and disinformation during the election cycle. These posted equivalent or reduced levels of support on average than in 2023.

Key Human Rights Proposals (excluding conservative versions)

Conservative Issues

Conservative-leaning investors—primarily the National Center for Public Policy Research (NCPPR) and the National Legal and Policy Center (NLPC)—upped the ante this year with a record 114 filings, compared to 103 in 2023. Because they often counter traditional ESG initiatives, their requests generally receive only single-digit support.

As in past years, their most successful resolution, sponsored by NLPC, called for an independent board chair. The proposal received 33.7% at Goldman Sachs Group, up from 16.4% in 2023 and 16.1% in 2022 when ISS opposed it. This year the measure was backed by both proxy advisors as well as Norges Bank Investment Management. A repeat resolution at Salesforce garnered 21.6% support, which has been declining since 2022 when the company appointed a lead independent director.

Conservative groups continued to focus most of their efforts on social issues, but this year more than doubled their volume of filings on climate change. These largely dealt with the feasibility, risks and economic impact of companies’ voluntary carbon reduction goals, which received a high of 8.1% at United Parcel Service. A new companion proposal from NLPC, which advised several energy and motor vehicle companies to delink executive pay from GHG reduction targets, faltered with an average of 1.1% support.

As in 2023, their most prevalent social themes addressed civil liberties and non-discrimination in the workplace and the risks of politicized debanking. Although the former topic failed to gain any additional traction this year, the ethical finance proposals inched up in average support to 2.2% from 1.2% in 2023. Notably, 10 states have enacted or are considering enacting fair access legislation which would prohibit financial institutions from denying or canceling services to a person based on factors, such as political opinions, religious beliefs or social credit scores, that are not quantitative, impartial and risk-based8.

Conservative-sponsored initiatives have traditionally fared better on human rights issues which have a broader appeal for some institutional investors. This year, proposals by New Breeze and NCPPR calling for audits of child labor in electrical vehicle supply chains achieved 12.8% support at General Motors and 5.6% at Ford Motor, though these tallies were down from prior years. The same resolution raised by NLPC at General Motors scored 22.4% in 2022 when ISS supported it, while the NCPPR resolution at Ford received 6.5% in 2023.

Key Conservative E&S Proposals

Governance Issues

Traditional Governance Topics

Shareholder proposals on traditional governance topics excelled this season, capturing 42 majority votes–the highest number since 2021. This was attributable to Chevedden and Steiner shifting their efforts to a measure that holds widespread appeal for investors: the elimination of supermajority voting provisions, which accounted for 31 of the successful resolutions and in 12 cases were not opposed by the boards.

The Chevedden group additionally scored four majority votes on resolutions to improve special meeting rights at companies that lacked such rights or had high ownership requirements (40%-50%) to invoke a special meeting. Five of their board declassification proposals also attained majority votes, including one that was unopposed by the board and one at Meritage Homes, which had already planned to sunset its staggered board by the conclusion of the 2027 annual meeting.

Additional majority votes for the second half of 2024 are already afoot. In July, three occurred, including board declassification at Snowflake and the adoption of special meeting rights at Autodesk and LL Flooring Holdings.

Two new proposal variations on independent board leadership and dual-class stock were presented at Meta Platforms this year, each of which received a little over 17% support and the backing of the proxy advisors. In order to provide more independent oversight of Chair/CEO Mark Zuckerberg, the United Church of Canada asked the company to amend its governance guidelines so that the board chair and lead director would have the ability to include items on board meeting agendas independent of each other. The Illinois State Treasurer also requested that Meta disclose voting results by each class of shares so that the Class A shareholders could better monitor how responsive the company is to their concerns. This was in addition to a longstanding proposal by NorthStar Asset Management and NYSCRF to recapitalize the Meta shares into one class, which received 26.3% support – the lowest level since 2019.

Director Resignation Policies

One of the most prolific resolutions this year, primarily sponsored by the UBC, endeavored to strengthen director resignation policies to prevent the occurrence of “zombie” directors who remain on the board after failing their election. The proposed measure would require director nominees to submit an irrevocable conditional resignation upon failure of election. If not accepted by the board and the director failed election the following year, he would be required to step down within 30 days after certification of the vote.

This was the first year the UBC resolutions reached proxy ballots after a similar campaign was abandoned in 2022. The eight proposals averaged 17.6% support and were opposed by ISS but backed by Glass Lewis. Nineteen proposals were successfully omitted as either a violation of state law or for inadequate proof of stock ownership, while another 14 were withdrawn, in some cases due to an ongoing dialogue with the company.

Chevedden and Steiner produced their own versions of this theme which would require the board to accept the resignation of a failed director or, alternatively, to refrain from renominating a failed director to the board. Two companies challenged the latter formulation as a violation of Delaware law, but the SEC did not concur. The five resolutions voted averaged 16% support and were similarly rejected by ISS but supported by Glass Lewis.

Apart from their prescriptiveness, the resolutions drew lackluster support because of their targeting. Although the occurrence of “zombie” directors is infrequent, the proponents failed to take aim at the small number of companies where directors have failed to obtain majority approval—in some cases for five to six consecutive years (TG Therapeutics and Avalon Holdings) – but remain on the board because of plurality voting or because the board has repeatedly rejected the director’s resignation (Ashford Hospitality Trust).

Key Governance Proposals

*Of the 2024 majority votes, one board declassification proposal, 12 supermajority voting proposals, and the proxy access proposal were not opposed by the board.

**Of the 2023 majority votes, five supermajority voting proposals were not opposed by the board.

***June 2024 votes on declassification proposals at three closed-end mutual funds have not yet been reported.

Officer Exculpation

For a second year, another wave of Delaware corporations asked their shareholders to approve charter amendments to extend certain liability protections to their officers which prior to August 2022 were only available to directors under the Delaware General Corporation Law (DGCL).

Through June, 307 officer exculpation proposals were presented in accordance with the DGCL—a 23% increase over the first half of 2023 when many companies held off in order to gauge investor and proxy advisor reaction. This included a more than doubling of proposals put forward by S&P 500 firms, along with a 36% uptick in proposals by multi-class stock companies following the January 2024 Delaware Supreme Court ruling (In re Fox Corporation/Snap Inc. Section 242 Litigation) that companies do not need to seek a separate shareholder class vote to approve charter amendments exculpating corporate officers. There were also about a half dozen repeat proposals from companies that failed to obtain shareholder approval of their provisions last year.

Of this season’s votes, only 29 failed (9.5%), which in 13 cases was due to supermajority voting requirements. This compares to a failure rate of 16% in the first half of last year.

As in 2023, proxy advisor recommendations had little bearing on voting outcomes. ISS has largely been supportive of these provisions (81%) except at companies whose governance structures limit accountability to shareholders, such the presence of controlling shareholders or multi-class voting stock. Glass Lewis has continued to oppose officer exculpation amendments on the basis that shareholders should not relinquish their right to sue corporate officers for claims of negligence and breaches of fiduciary duty of care. It will make an exception if the company provides a compelling rationale for adopting it, which occurred in one case this season—WESCO International. The company argued that because an increasing number of Delaware companies have adopted exculpation provisions, not having one could impair its ability to compete for executive talent due to concerns about exposure to personal liability.

Compensation Issues

Severance Pay

Chevedden and Steiner pared back their severance pay proposals after sponsoring 50 of the 52 filed in 2023, which generated 23.6% in average support and four majority votes. Their 2024 resolutions, which called for shareholder approval of golden parachute payments in excess of 2.99 times base salary and short-term bonus, varied in terms of whose pay packages were covered—the top 10 managers, named executive officers (NEOs) or Section 16 officers.

As in 2023, the votes were widely scattered—ranging from single-digit to a high of 41.7%–based on whether or not the company had already adopted a policy in line with the proponent’s request and proxy advisor policies. Because most of the targets had done so, average support for the 30 proposals voted in 2024 dropped to 15.5%.

Director Pay

Chevedden teamed up with Michael Levin, founder and editor of The Activist Investor, to submit 13 binding bylaw resolutions to require shareholder pre-approval of directors’ compensation. The idea came about from a proposed settlement of a derivative lawsuit alleging that Tesla’s directors overpaid themselves from 2017 to 2020. In addition to returning $735 million in cash and equity awards to the company, the board would be required to provide an annual shareholder vote on director pay for a period of five years.

Over half of the targeted companies were able to omit the “say on director pay” resolution as a violation of state law or as micromanagement. The five voted attracted only 2% in average support and were opposed by the proxy advisors.

Living Wage

The Shareholder Commons, along with Legal & General Investment Management and various religious orders, sustainable investment funds and individuals, undertook a new initiative this year aimed primarily at retailers to pay workers a living wage.

Of the eight proposals submitted, seven were challenged as ordinary business and no-action relief was granted depending on how the resolution was framed. Those deemed to constitute micromanagement asked for a living wage report detailing compliance with international human rights standards and data on the number of employees being paid less than a living wage. Those calling for the establishment of a compensation policy to provide workers with a living wage were not excludable because they addressed the broader societal issues of wealth inequality and racial/gender disparities.

In view of the SEC’s decisions, McRitchie plans to file more of the latter type of proposal later this year and next year. The four that came to a vote this season averaged only 10.9% support and were rejected by ISS and Glass Lewis.

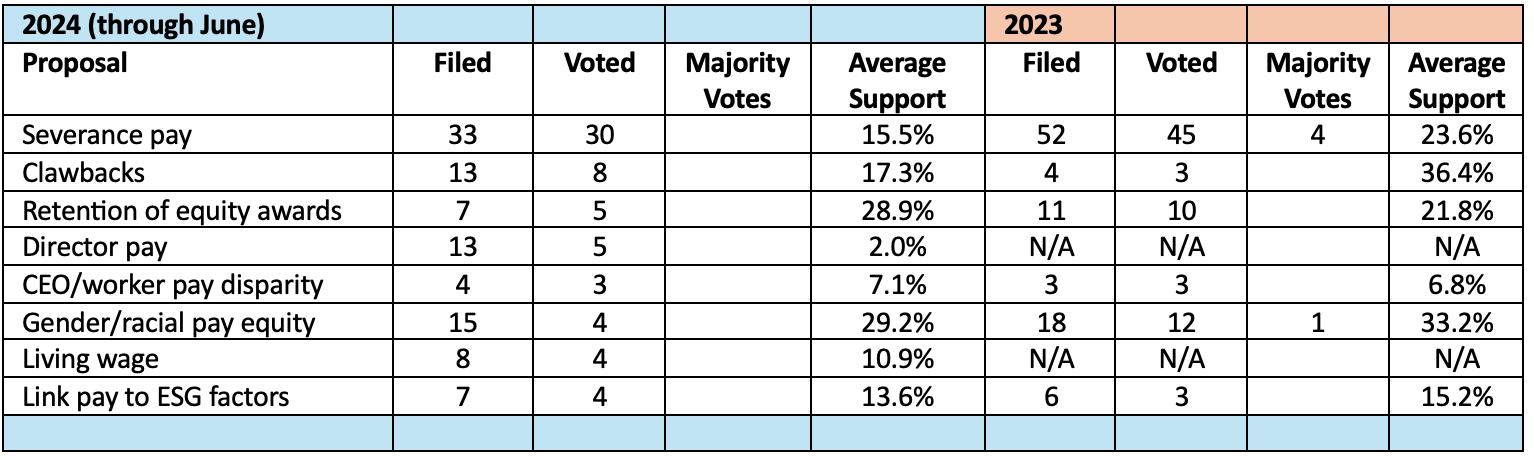

Key Compensation Proposals

Say on Pay

Investors showed strong support for management SOP proposals this season with votes across all U.S. public companies averaging 91%, compared to 89.7% in the first half of 2023. This year’s failure rate (1.3%) was down significantly from last year (2%) and the lowest level since 2017. Similarly, the proportion of companies receiving less than 70% SOP support (6.1%) was substantially less than in the 2023 proxy season (7.4%).

Of the 35 failures through June of this year, 27 were among Russell 3000 firms, including four in the S&P 500 index—3M, Norfolk Southern, Salesforce and Zebra Technologies. Last year’s 56 failures encompassed 45 Russell 3000 companies, including 11 S&P 500 constituents. Thirteen of this year’s failed votes had occurred in prior years, compared to 20 repeat failures during the first half of 2023. The most common investor concerns behind the 2024 failures were pay-for-performance misalignment, the rigor of performance goals, and problematic pay practices.

The improved SOP results relative to 2023 reflect a lower incidence of negative ISS recommendations as well as effective engagement between issuers and investors. Only 12.1% of firms received an “against” opinion from ISS, compared to 13.1% during the first half of last year. Even in the face of ISS opposition, average SOP support reached 72.9%, versus 69.6% in 2023, suggesting that investor votes have become less aligned with ISS’s opinions.

SOP Vote Trends

Pay-for-Performance Win

Elon Musk received a vote of confidence from Tesla shareholders, who decisively re-ratified his 2018 incentive pay award, worth nearly $50 billion, after a Delaware Chancery Court voided it in January as excessive and for being approved by a conflicted board. The second shareholder confirmation of the package could strengthen Tesla’s efforts to appeal the ruling since investors have now been fully informed about the process.

The pay package was approved by 72% of the disinterested voting shares—nearly the same proportion as in 2018 (73%)–suggesting that many of the shareholders who endorsed it six years ago stood by their original decision. Vanguard, which had opposed the option grant in 2018, switched to supporting it this year, citing the strong alignment of the compensation with the company’s performance and associated shareholder returns, which have significantly outperformed the market since 20189.

Shareholders also approved the company’s reincorporation from Delaware to Texas, where Tesla is headquartered, on the basis that shareholder rights would not be materially impacted. Texas is opening specialized business courts in September and is planning to launch a new national stock exchange to rival the NYSE and Nasdaq.

Regulatory Uncertainty Ahead

Pending litigation, court rulings and the upcoming presidential election have led to a challenging but potentially favorable regulatory environment ahead for issuers. Alongside proxy season, the following developments occurred.

SEC Rulemaking Delayed

The SEC has delayed key rulemaking activity until after the fall elections, according to its Spring 2024 Regulatory Flexibility Agenda, released in early July10. Proposed rules on human capital management disclosures and on financial institutions’ incentive-based compensation arrangements are now scheduled for October 2024, as is a final disclosure rule to prevent greenwashing in ESG and similarly labeled funds. A proposed rule on corporate board diversity and a final rule amending Rule 14a-8’s substantial implementation, duplication and resubmission exclusions of shareholder proposals have been pushed back to April 2025. These are estimated timetables that could change significantly post-election.

Climate Change Rules on Hold

In April, the SEC delayed implementation of its climate disclosure rule pending the outcome of litigation in the U.S. Court of Appeals for the Eighth Circuit. The rule, which was finalized in March, requires registrants to provide a comprehensive set of disclosures covering material climate-related risks and their impacts on the company, board oversight of climate-related risks, material Scope 1 and Scope 2 emissions accompanied by an attestation report, and any climate-related targets and goals, scenario analyses, internal carbon pricing and transition plans that the company has adopted.

Because a final judgment could extend beyond 2025, the SEC may have to push back the rule’s initial compliance date (2026) if it prevails in the litigation in order to give issuers more time to prepare. In the interim, if the fall elections result in a Republican administration, the rule could be scaled back or scrapped entirely. Either way, companies should expect continued investor pressure to voluntarily provide climate-related disclosures.

Meanwhile, California Governor Gavin Newsom has proposed a two-year delay in the implementation of the state’s climate laws, which were enacted in 2023. If amended, Senate Bill 253 would require companies doing business in California with over $1 billion in revenue to report their Scope 1 and Scope 2 emissions in 2028 and to report their Scope 3 emissions in 2029. Under an amended Senate Bill 261, companies with over $500 million in revenue would begin reporting climate-related financial risks based on the Task Force on Climate-Related Financial Disclosures (TCFD) framework in 2028. Although the laws are facing legal challenges, the revised timetable was caused by the inability of the California Air Resources Board to develop the implementing regulations by Jan. 1, 2025.

Board Diversity Rule in Limbo

The U.S. Court of Appeals for the Fifth Circuit is rehearing en banc a lawsuit challenging Nasdaq’s board diversity rule. The rule, which was approved by the SEC in August 2021, requires listed companies to disclose details about their board diversity and, beginning Dec. 31, 2025, to have a minimum of two directors who self-identify as diverse in terms of gender, race, or LGBTQ+ status, or to explain why they do not. The petitioners claim that the rule it is an unconstitutional violation of equal protection and free speech rights and that the SEC’s approval of it violates the Securities Exchange Act of 1934 and the Administrative Procedure Act.

Potential Reinstatement of Proxy Advisor Rules

In late June, the Fifth Circuit Court of Appeals struck down the SEC’s rescission of Trump Administration rules requiring proxy advisory firms to provide their voting advice to their clients and companies at the same time and to allow their clients to view the companies’ comments. An additional lawsuit by business groups against the SEC is pending in the Sixth Circuit. If that court reaches a similar decision, the notice-and-awareness requirements could be reinstated.

SCOTUS Limits Federal Agency Powers

Prior to the end of its 2024 session, SCOTUS issued a flurry of landmark decisions that rein in the administrative state by making it easier for businesses and other parties to challenge federal regulations, including some that are long-established. The decisions include:

- SEC v. Jarkesy: Guarantees the right to a jury trial for parties charged with regulatory violations that entail financial penalties, thereby curtailing the use of agency administrative proceedings.

- Corner Post, Inc. v. Board of Governors of the Federal Reserve System: Eases the six-year statute of limitations for challenging agency rulemaking, which will begin to run when the plaintiff is first injured by the rule, not when the rule is published.

- Loper Bright Enterprises v. Raimondo: Ends Chevron deference so that the judiciary, rather than federal agencies, has the ultimate authority to interpret ambiguous laws enacted by Congress.

Loper Bright is already facing its first test in an ESG context. Following the SCOTUS ruling, the Fifth Circuit Court of Appeals ordered the U.S. District Court for the Northern District of Texas to reconsider a lawsuit by over two dozen states challenging the 2022 Department of Labor (DOL) rule that permits retirement plan fiduciaries to consider ESG factors when selecting investments. The lower court’s original decision in favor of the DOL had focused on the Chevrondoctrine.

With many dynamics at play, Alliance Advisors will continue to monitor significant developments that arise to assist issuers in their fall engagements and preparations for the 2025 annual meeting season.

[1] See also the Shareholder Rights Group’s report on no-action requests from Nov. 1, 2023, to May 1, 2024, at https://www.shareholderrightsgroup.com/2024/05/sec-no-action-statistics-for-2024.html?m=1.

[2] See, for example, T. Rowe Price Associates’ review of its 2023 proxy votes at https://www.troweprice.com/content/dam/trowecorp/Pdfs/For_or_Against_Shareholder_Resolutions.pdf.

[3] See Jamie Dimon’s 2024 letter to shareholders at https://reports.jpmorganchase.com/investor-relations/2023/ar-ceo-letters.htm.

[4] See Orrick’s report at https://www.orrick.com/en/Insights/2024/06/AI-Disclosures-in-SEC-Filings-Trends-From-the-S-and-P-500.

[5] According to Farient Advisors’ review of 1,200 firms, the proportion using DEI factors to set executive compensation has dropped to 28% from 33% in 2023. See https://farient.com/2024/07/03/momentum-shift-dei-metrics-role-wanes/.

[6] See the 2023 CPA-Zicklin Index of Corporate Political Disclosure and Accountability at https://www.politicalaccountability.net/wp-content/uploads/2024/06/2023-CPA-Zicklin-Index.pdf.

[7] Following the June 2024 SCOTUS decision allowing for continued access to the abortion pill mifepristone, the New York City Comptroller and 54 Democrat members of Congress urged the CEOs of five major pharmaceutical companies to immediately begin dispensing the drug in states where it is legal. Medication abortion accounts for 63% of all abortions in the healthcare system. See https://comptroller.nyc.gov/newsroom/nyc-comptroller-presses-pharmacy-giants-to-provide-abortion-medication-or-risk-losing-investor-confidence/ and https://goldman.house.gov/sites/evo-subsites/goldman.house.gov/files/evo-media-document/7.2_MifeLetter_FINAL.pdf.

[8] Florida and Tennessee have enacted fair access statutes. Arizona, Georgia, Idaho, Indiana, Iowa, Kentucky, Louisiana and South Dakota are considering similar legislation. See Sullivan & Cromwell’s related memo at https://www.sullcrom.com/SullivanCromwell/_Assets/PDFs/Memos/States-Require-Fair-Access-Financial-Services.pdf.

[9] See Vanguard’s vote bulletin on Tesla at https://corporate.vanguard.com/content/dam/corp/advocate/investment-stewardship/pdf/perspectives-and-commentary/tesla_insights.pdf.

[10] See the SEC’s Spring 2024 Reg Flex Agenda at https://www.reginfo.gov/public/do/eAgendaMain?operation=OPERATION_GET_AGENCY_RULE_LIST¤tPub=true&agencyCode&showStage=active&agencyCd=3235.

Alliance Advisors has built a team of industry specialists with deep experience relating to all our product lines. If you would like to receive a copy of our reports and reviews in future, please enter your details in the form below.