How Digital Tools Have Become the New Standard in Mutual Fund Proxy Solicitations

Sam Chandoha

Every mutual fund—or any company with a retail-heavy shareholder base—faces the same reality: achieving quorum or higher vote thresholds at a shareholder meeting is both difficult and expensive. Mutual fund shareholder demographics are remarkably consistent across fund groups: large numbers of retail investors holding relatively small dollar-value positions, dispersed across intermediaries and account types. Whether a shareholder holds shares in street name or is registered makes little difference—the underlying demographic challenge remains the same.

Compounding this issue, the NOBO/OBO framework allows a fund to identify only roughly half of its street-name shareholders, which significantly limits direct outreach. In addition to the sheer volume of small positions, many retail investors are less familiar with the governance requirements of mutual funds and may not recognize that shareholder approval is required for certain matters, such as advisory agreements or board elections. The result is a persistent pattern of low engagement: a large population of shareholders who do not prioritize voting and often ignore traditional proxy mailings.

This challenge is further amplified in solicitations involving ETFs and money market funds, where shareholders frequently move in and out of positions. An investor may technically be a holder of record on the record date but may no longer own the fund during the solicitation period and therefore feel little incentive to participate in the vote.

These issues are not new. However, two structural developments have turned what was once a manageable challenge into a more complex and costly undertaking: the disappearance of landline telephones from most households and the dramatic expansion of mutual fund ownership across the investing population.

Historical Solicitation Strategies

Outbound Telephone Campaigns

For many years, a typical mutual fund solicitation followed a predictable pattern. Fund groups would mail proxy materials to all shareholders, wait for approximately 25 percent of the votes to be returned, and then engage a proxy solicitor to launch an outbound telephone campaign. The introduction of telephone voting by Shareholder Communications Corporation in the 1990s significantly improved this process: call-center agents could reach shareholders at home, walk them through the voting process, and complete a vote in under two minutes. With a call center staffed by 200 agents, a proxy solicitor could contact approximately 20,000 shareholders during a single evening shift.

Today, that model faces substantial headwinds. The widespread adoption of mobile phones, combined with the abandonment of landline service in most households, has reduced the effectiveness of outbound calling. While telephone outreach is still used and continues to generate some votes, it can no longer be relied upon to bridge the gap between votes returned by mail and votes required for approval. Where agents once completed as many as 22 calls per hour, that number has dropped to roughly six to eight, as shareholders increasingly decline to answer calls from unfamiliar numbers or screen heavily against perceived spam. Even when fund groups possess mobile numbers, reachability and connection rates have declined.

The Explosion of Fund Ownership

The growth of mutual fund ownership has further strained traditional solicitation models. Since the introduction of IRAs in the late 1970s and the subsequent rise of 401(k) and other defined contribution plans, mutual fund ownership has expanded across a broad segment of U.S. households. According to estimates from the Investment Company Institute, there are now more than 115 million mutual fund accounts in the United States. As a result, when a large fund group conducts a proxy solicitation, it may involve millions of shareholders—most of whom historically do not vote and therefore require active solicitation.

The scale of these efforts has direct cost implications. For example, a fund group with three million shareholders could reasonably expect to budget between 10 million and 20 million dollars for a large solicitation, depending on the proposals under consideration, and the mix of communication channels. Every action carries a cost, and even a basic reminder mailing can reach into the millions. A solicitation that relies too heavily on a narrow set of tactics, or that does not adjust to changing shareholder behavior, can result in substantial incremental spend with limited additional voting returns.

Digital Tools Deliver Votes¹

There is no single solution to retail shareholder engagement, and different shareholder segments respond to different approaches. Nonetheless, many proxy solicitation programs have historically leaned on a uniform playbook: mail, remail, and repeated outbound calling. In an environment where landlines are disappearing and digital communication is ubiquitous, that model is increasingly difficult to sustain on its own.

Alliance Advisors has developed a suite of digital tools designed to complement traditional solicitation methods and, in many situations, to extend or enhance their effectiveness. For larger or more complex shareholders, outbound telephone outreach remains a useful tactic. For smaller, harder-to-reach, or historically unresponsive shareholders, targeted digital channels—such as text messaging and branded email campaigns—provide additional touch-points that align more closely with how investors communicate today. This hybrid strategy can be more cost-effective and has the potential to generate vote returns even after traditional telephone campaigns have reached diminishing marginal results.

Case Study: Digital Tools in Practice

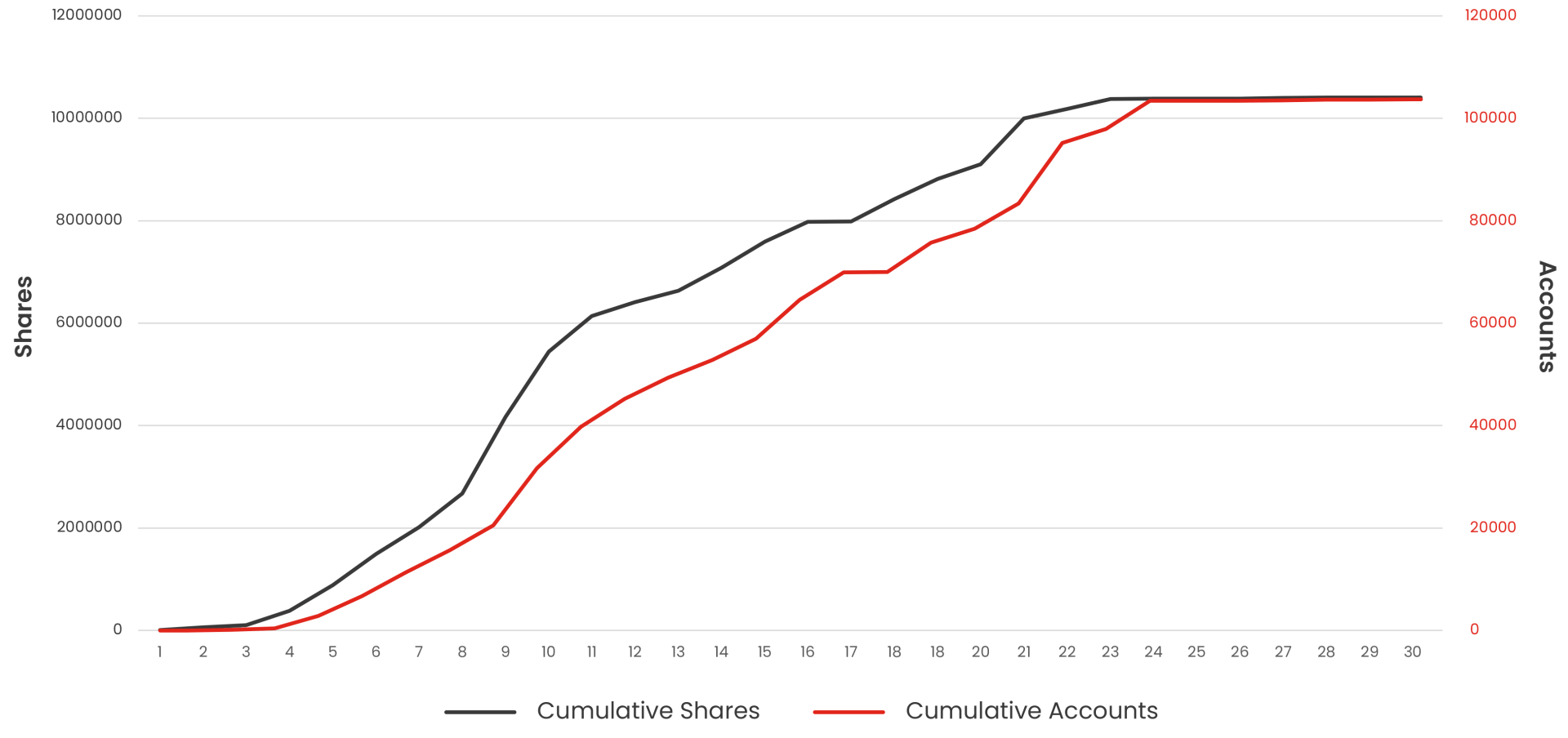

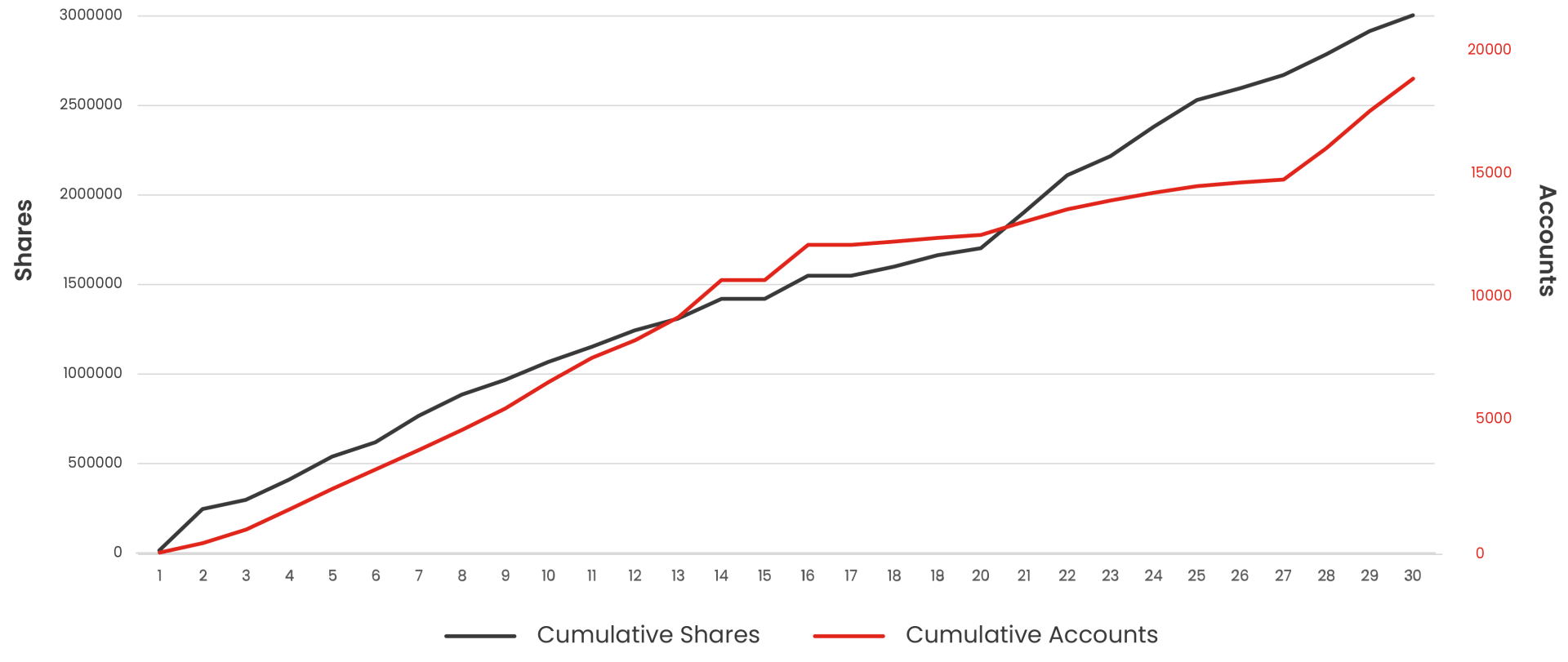

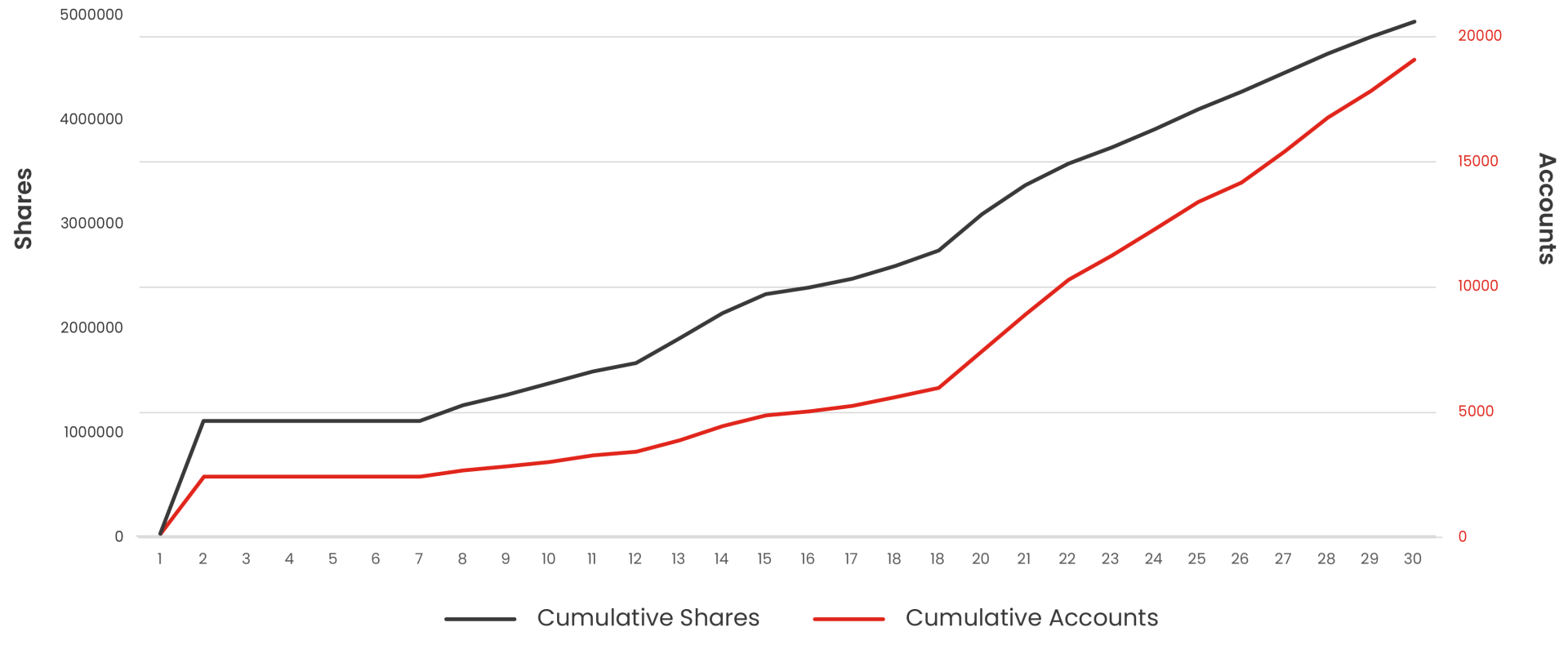

Alliance Advisors was engaged to assist with a large-scale mutual fund solicitation involving approximately 5,000,000 shareholders. The fund company had previously retained another proxy solicitor that, after one adjournment and more than 60 days of activity, had achieved only 38 percent of the outstanding shares voted, despite a requirement to reach 50 percent. At that point, the outbound call campaign had largely run its course and was generating minimal daily vote movement. With 30 days remaining before the deadline, Alliance Advisors was retained with a clear mandate: deploy a broad suite of digital tools to re-engage shareholders and restart vote momentum.

The objective was not to abandon traditional methods but to add complementary channels that could more effectively reach shareholders who were not responsive to previous outreach. It is important to note that no single tool operated as a standalone solution or “magic bullet”. Each tactic produced measurable results on its own, but the most meaningful impact came from a coordinated, phased strategy designed to reach different shareholder segments at different points in the solicitation.

Below, is an overview of each of the digital tools that were used during this engagement to deliver the majority vote needed and a successful outcome.

Text to Vote™

Given widespread reluctance to answer unknown phone calls, Text-to-Vote™ has emerged as an effective way to capture shareholder attention—particularly among younger investors who prefer to transact via mobile devices. This approach allows Alliance Advisors to send shareholders a concise SMS or MMS text message containing an embedded, secure link that directs them to a voting page. Registered and NOBO shareholders can review key information and vote quickly and conveniently from their phones.

In this case study, Text-to-Vote™ accounted for 33.3 percent of the total votes captured during the solicitation. While the relative contribution of text messaging will vary by shareholder base and data quality, these results indicate that text can be a significant driver of incremental participation when integrated into a broader strategy.

Email Voting

Email voting operates on a similar principle but allows for a more detailed communication than text. Branded email messages are delivered to registered, OBO, and NOBO shareholders and include direct voting links that enable participation in just a few clicks. Unlike traditional mail, email provides immediate delivery, clear calls to action, and the ability for shareholders to vote without printing, signing, or mailing a proxy card.

In the solicitation described above, Email Voting represented 37.9 percent of the total votes captured. For shareholder populations with reliable email coverage, this channel can serve both as a primary method of engagement and as a reinforcement to other outreach, particularly when reminders are sequenced over time.

Proxy Lite

Proxy Lite is designed to address the same core challenge facing traditional outbound calling: shareholders’ reluctance to answer calls from unfamiliar numbers. In this approach, shareholders receive a prerecorded message asking them to call a toll-free number regarding their investment. When they return the call, they are connected to a live agent who can review the proposals and record their vote. If the shareholder answers the initial call, they can press“1” to be routed immediately to an agent.

In the case study, Proxy Lite accounted for 11.1 percent of the total votes captured. While this channel still relies on voice communication, it inverts the dynamic by prompting shareholders to initiate the contact, which can reduce the friction associated with unsolicited calls.

QR Code Mailings

QR Code Mailings are targeted communications sent late in the solicitation cycle to the largest unreachable or still-unvoted shareholders. These mailings are more targeted than standard mailings and focus on large, unvoted positions. This makes them an efficient tool for closing the gap in the final days of a solicitation. By combining physical mail with digital and telephone options, this approach offers a clear, time-sensitive call to action at a critical stage.

In this campaign, QR Code Mailings represented 18.2 percent of the total votes captured. Although they are more targeted and often more expensive on a per-piece basis than standard mailings, their focus on large, unvoted positions can make them an efficient tool for closing the gap in the final days of a solicitation.

The Common Thread: Immediacy and Accessibility

Across all these engagement strategies, a consistent theme emerges: immediacy. Digital tools provide shareholders with the ability to review key information and vote almost instantly, using channels they already rely on in their daily lives. Without simple, fast, and accessible voting options, many shareholder interactions fail to translate into actual votes, especially among those who are neutral or mildly supportive but not motivated to overcome procedural friction.

Conclusion

Alliance Advisors has been deploying digital solicitation tools for more than a decade, but their role in mutual fund proxy campaigns has changed meaningfully as shareholder communication habits have evolved. In an environment marked by reachability challenges, declining landline usage, and changing expectations around convenience, digital tools have become a central component of many successful solicitation strategies, rather than a peripheral add-on.

Digital channels can deliver votes at every stage of the solicitation cycle, particularly in later phases when traditional methods have been exhausted and timelines are compressed. They can be implemented relatively quickly, scaled efficiently, and configured in a cost-conscious way when integrated with data-driven targeting and clear messaging.

The effective use of these tools is both an art and a science which require a nuanced understanding of shareholder behavior, regulatory obligations, and operational constraints. Alliance Advisors’ experience across numerous corporate and mutual fund solicitations indicates that a well-designed digital program—paired with traditional tactics where appropriate—can help funds meet their voting objectives while managing cost and mitigating execution risk.

This article first appeared on the Ignites website HERE.

Copyright © 2026 F.T. Specialist Inc. All rights reserved.